ESRS After the Omnibus: From Volume to Pragmatism, From Fragmentation to Convergence

A Fundamental Shift in Banking Supervision

The European Commission’s 2025 Omnibus proposal to simplify the Corporate Sustainability Reporting Directive (CSRD) and its European Sustainability Reporting Standards (ESRS) marks a pivotal moment for corporate and financial leaders. While the changes promise a significant reduction in the reporting burden for companies, they simultaneously create a more fragmented and complex data environment for the banks, investors, and asset managers who rely on this information for risk management, product classification, and investment analysis. ESG Book’s latest executive briefing outlines the dual impact of this shift from volume-to- judgment, detailing what the changes mean for both corporate preparers and financial data users.

For Corporate Preparers: A Welcome Simplification

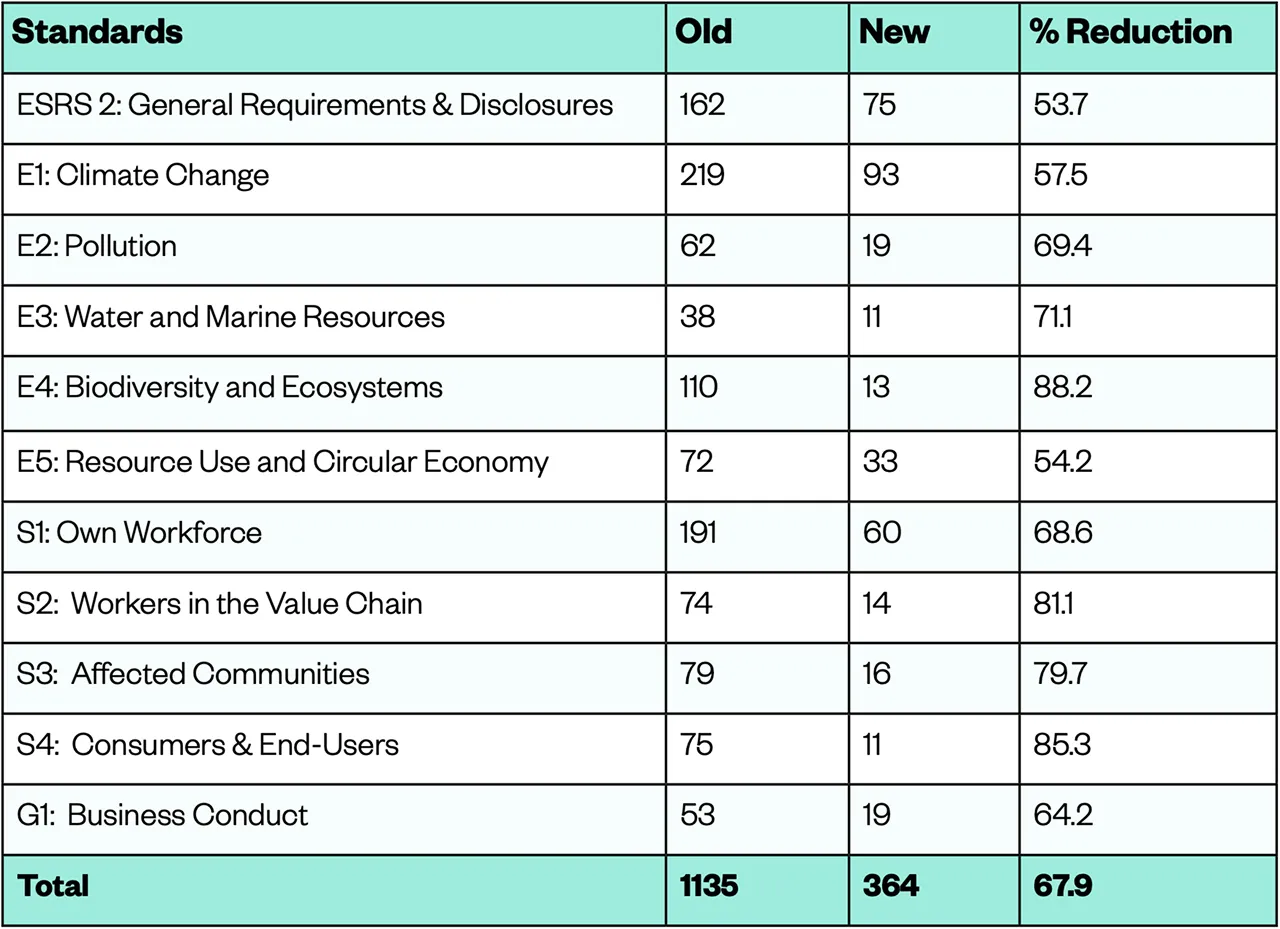

For reporting entities, the primary benefit of the ESRS revisions is a significant reduction in the reporting burden, moving the focus from exhaustive data collection to more strategic, principles-based disclosure. EFRAG estimates that the number of mandatory data points will decrease by approximately 61%, leading to reporting cost reductions of 28% in 2027, stabilizing at 33-36% from 2029.

The structural changes are even more significant:

For Financial Actors: A New Era of Fragmentation

While the simplification is a welcome change for reporters, it comes at a cost for the financial institutions that are the primary users of ESRS data. The revisions dilute the data foundation upon which ESG analysis, product classification, and risk management have been built since 2023.

Three consequences are particularly noteworthy:

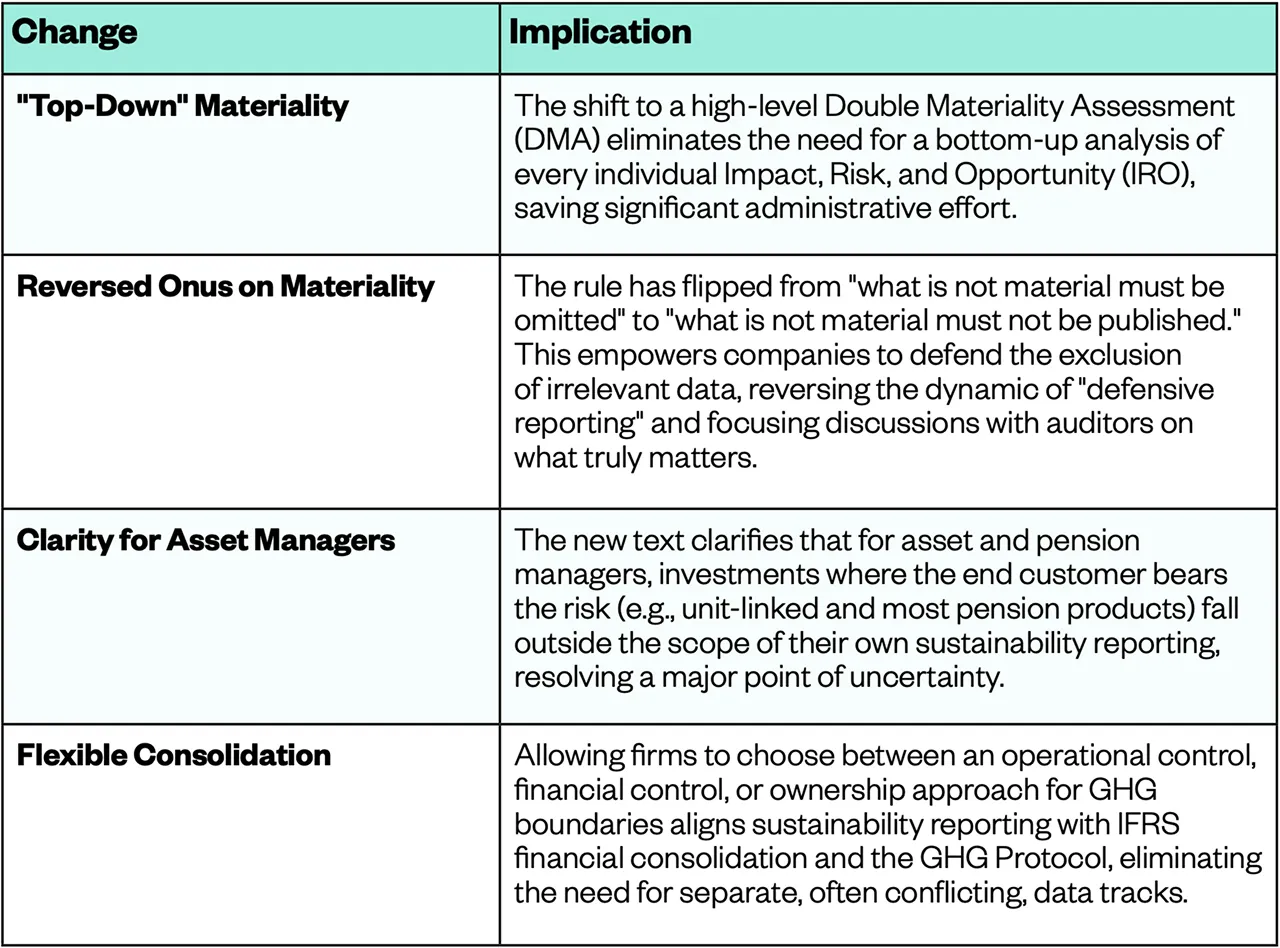

Key Comparative Metrics Disappear

The deletion of mandatory GHG and energy intensity ratios (per turnover) is a major setback. As the ECB and EBA have noted, these are the exact metrics used for Pillar 3 ESG reporting, financed emissions calculations (PCAF), and Green Asset Ratio (GAR) assessments. A bank seeking to compare the CO2 intensity of two borrowers will soon lack a standardized figure to do so, forcing a reliance on qualitative judgment over comparable metrics.

The Link Between Corporate Action and Financial Products is Broken

The revised standards weaken the direct link between a company’s transition plan and its financial proof points. By removing the requirement for a climate plan to reference Taxonomy-aligned CapEx or disclose its PAB exclusion status, the data chain is broken. An SFDR Article 9 fund manager, who could previously rely on standardized ESRS data, must now assemble these pieces independently, moving from a position of reliance to one of verification.

A Shift to Qualitative and Less Verifiable Disclosure

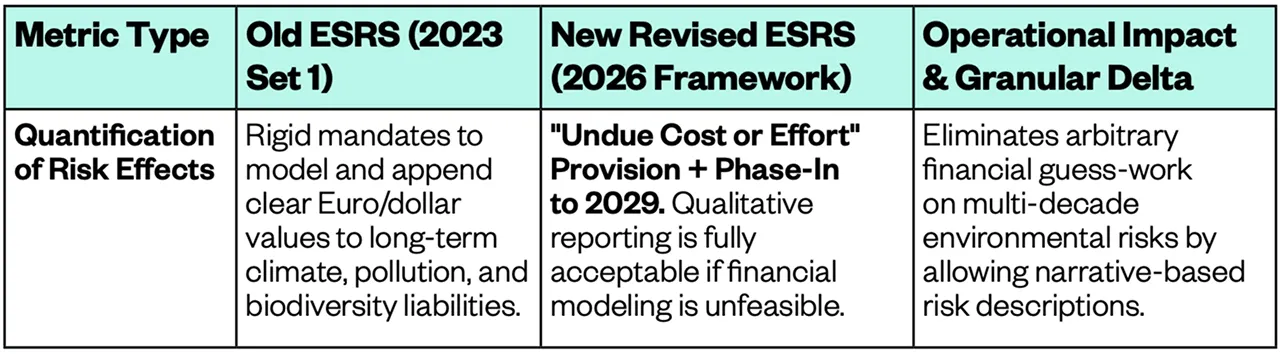

The overarching trend is a move from rigid quantitative metrics toward qualitative narratives. The requirement to quantify the financial effects of climate risks has been softened with phase-ins and “undue effort” exemptions. This shift to subjectivity complicates systematic risk assessment and automated data processing, confirming the concerns raised in EFRAG’s own user survey: 67% of investors expect the revised standards will reduce information quality, with 52% anticipating poorer comparability and 45% specifically pointing to the loss of critical climate data.

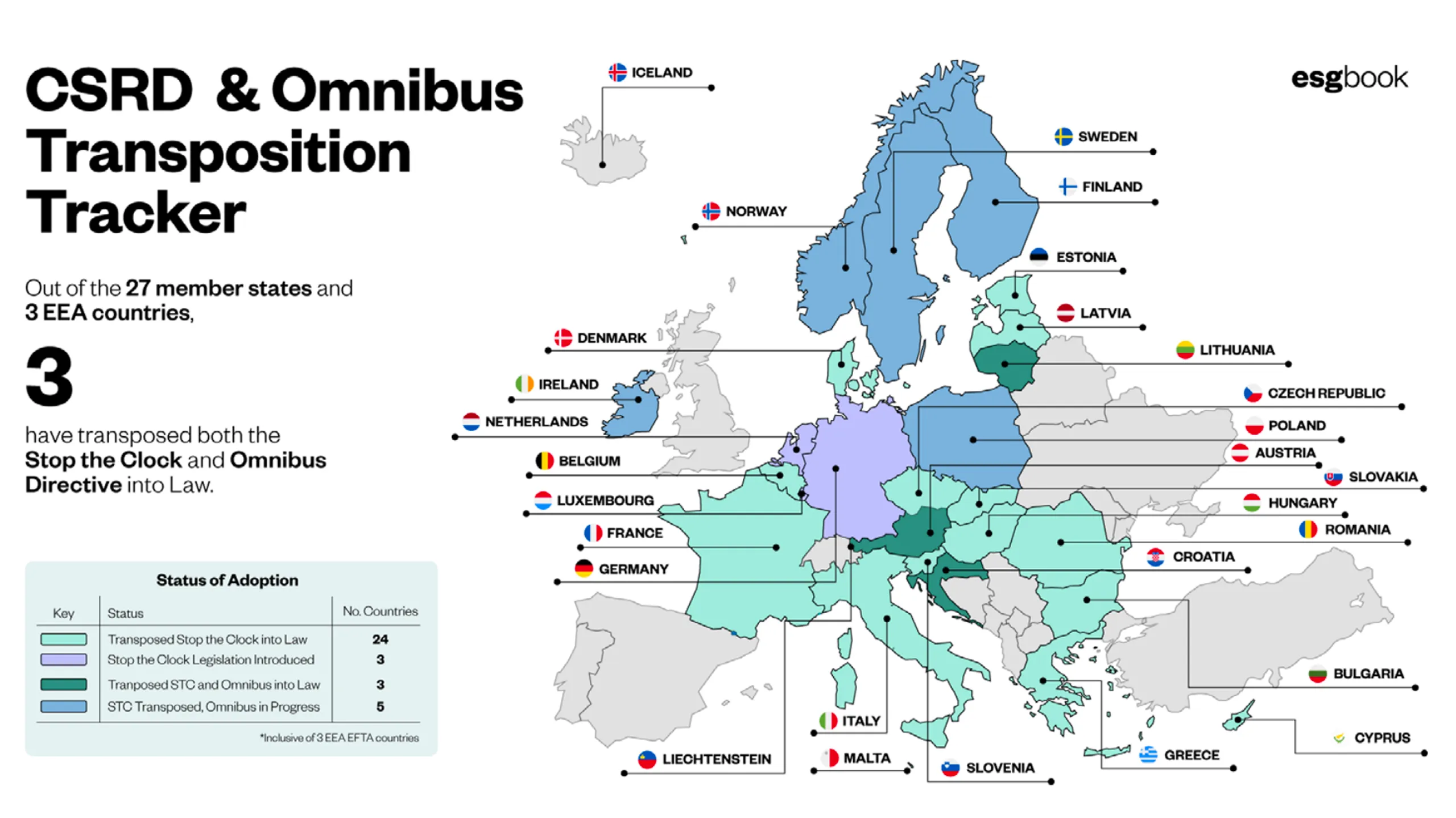

ESG Book’s CSRD/Omnibus Tracker

ESG Book’s CSRD/Omnibus Transposition Tracker is updated weekly to reflect the latest regulatory developments and the status of transposition progress by member states. The tracker covers both directives introduced as part of the European Commission’s Omnibus Proposal in February 2025. This includes the Omnibus I directive, which introduced substantive reforms to the CSRD framework, including revised scoping thresholds and reduced reporting requirements, with member states given until March 19, 2027, to transpose its provisions into national law. It also covers the “Stop the Clock” directive, which extended CSRD reporting deadlines by two years with a transposition deadline of December 31, 2025.

Conclusion

The revised ESRS framework marks a pivotal move toward a more principles-based reporting regime. For reporting companies, this brings a welcome focus on judgment and materiality. However, for the banks, asset managers, and pension funds that depend on this data, it signals a new era of fragmentation. These institutions will need to develop more sophisticated in-house analytical capabilities to navigate the less standardized and more qualitative landscape of corporate sustainability reporting.

The consultation period for these significant changes closes on 3 June 2026. If you rely on ESRS data for risk management or product classification, understanding the outcome of this regulatory simplification is critical.

Annex

A side-by-side granular layout shows the operational differences between the Old ESRS Set 1 (2023) and the Revised ESRS (2026 Omnibus Framework) across all 12 standards.

This comparative breakdown details exactly what has changed at the disclosure and metric level, mapping the structural shift toward an interoperable, principles-based regime.

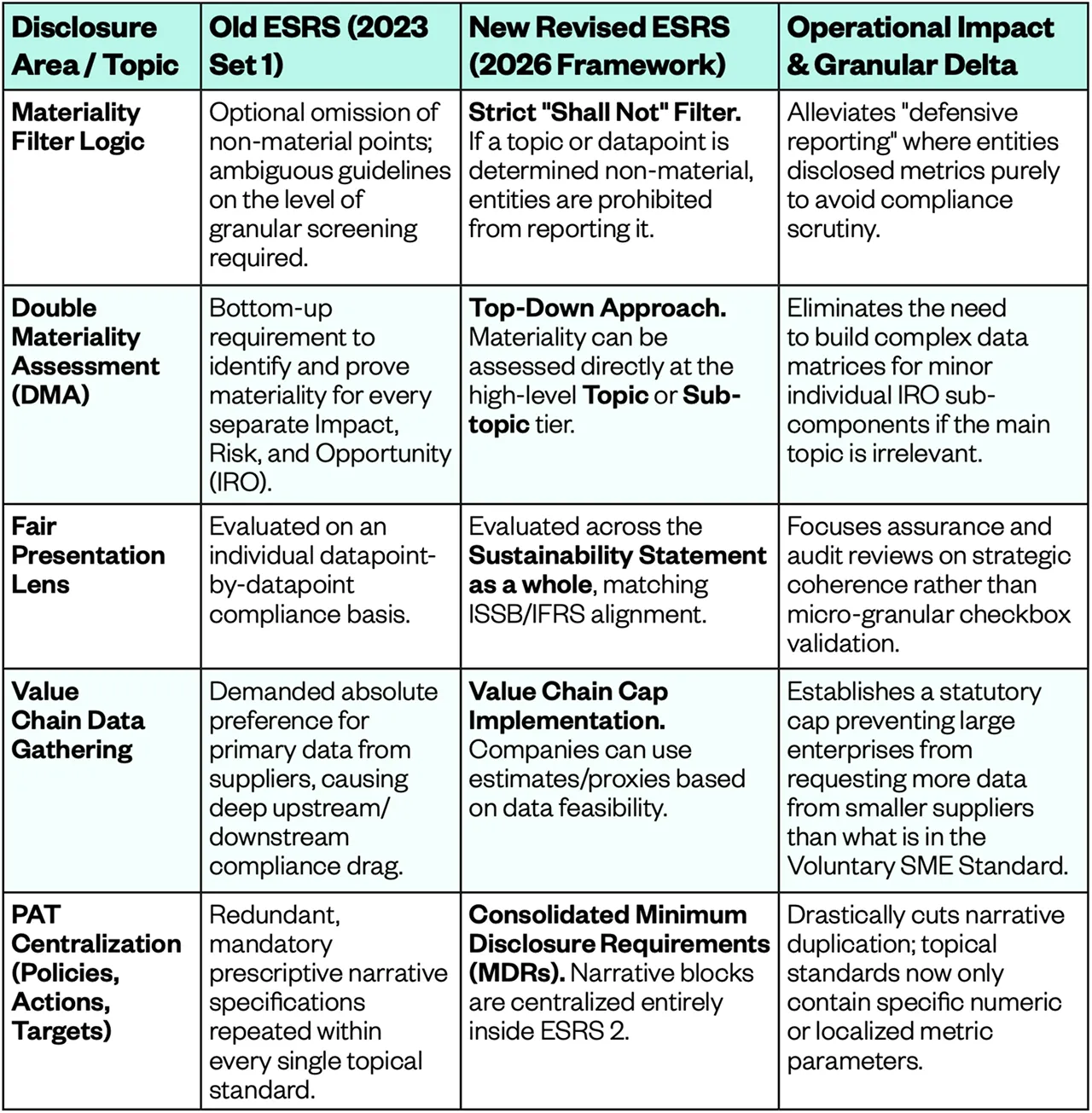

Cross-Cutting Standards

ESRS 1 & ESRS 2: General Requirements & Disclosures

Environmental Standards (E-Series)

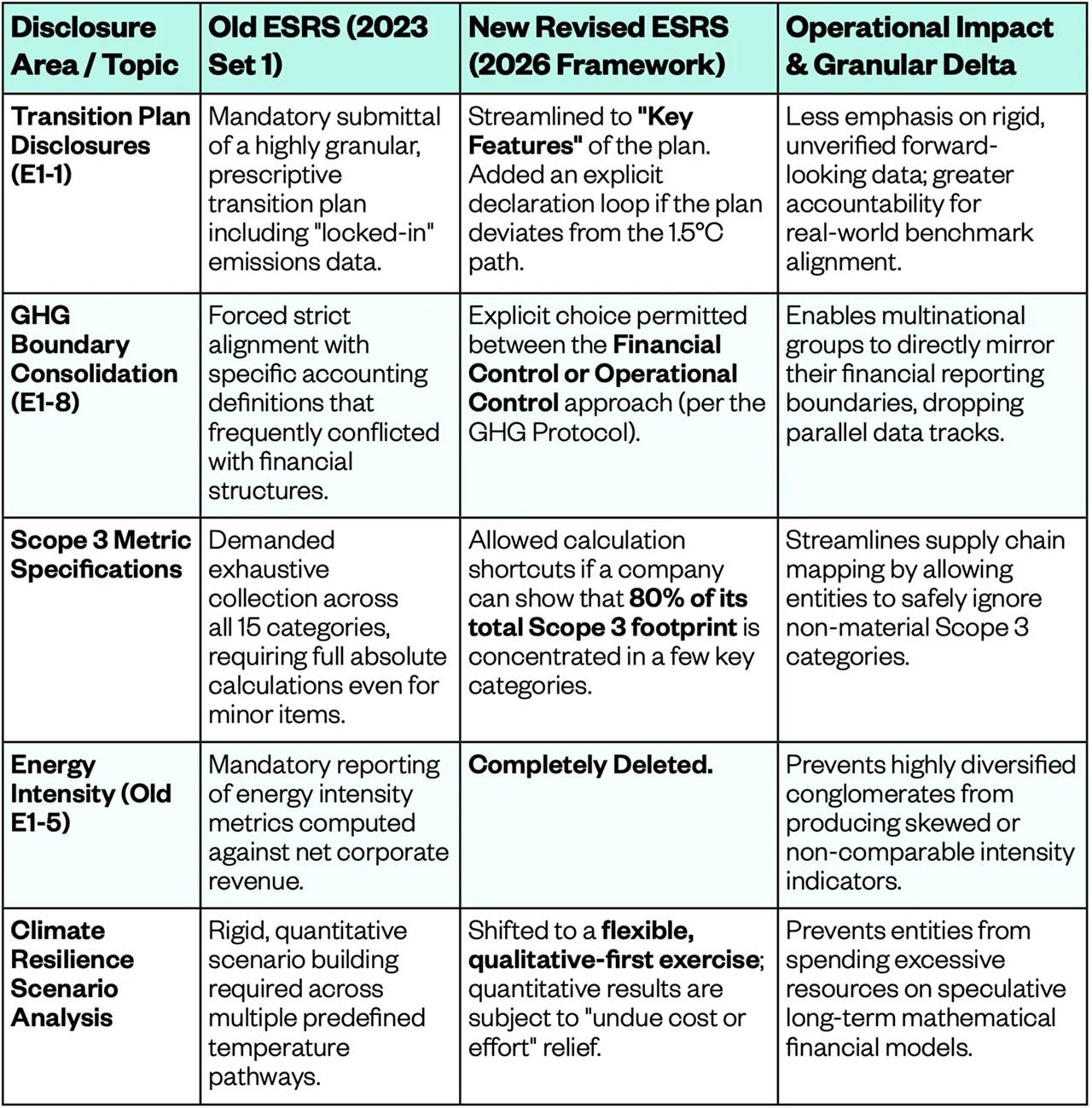

ESRS E1: Climate Change

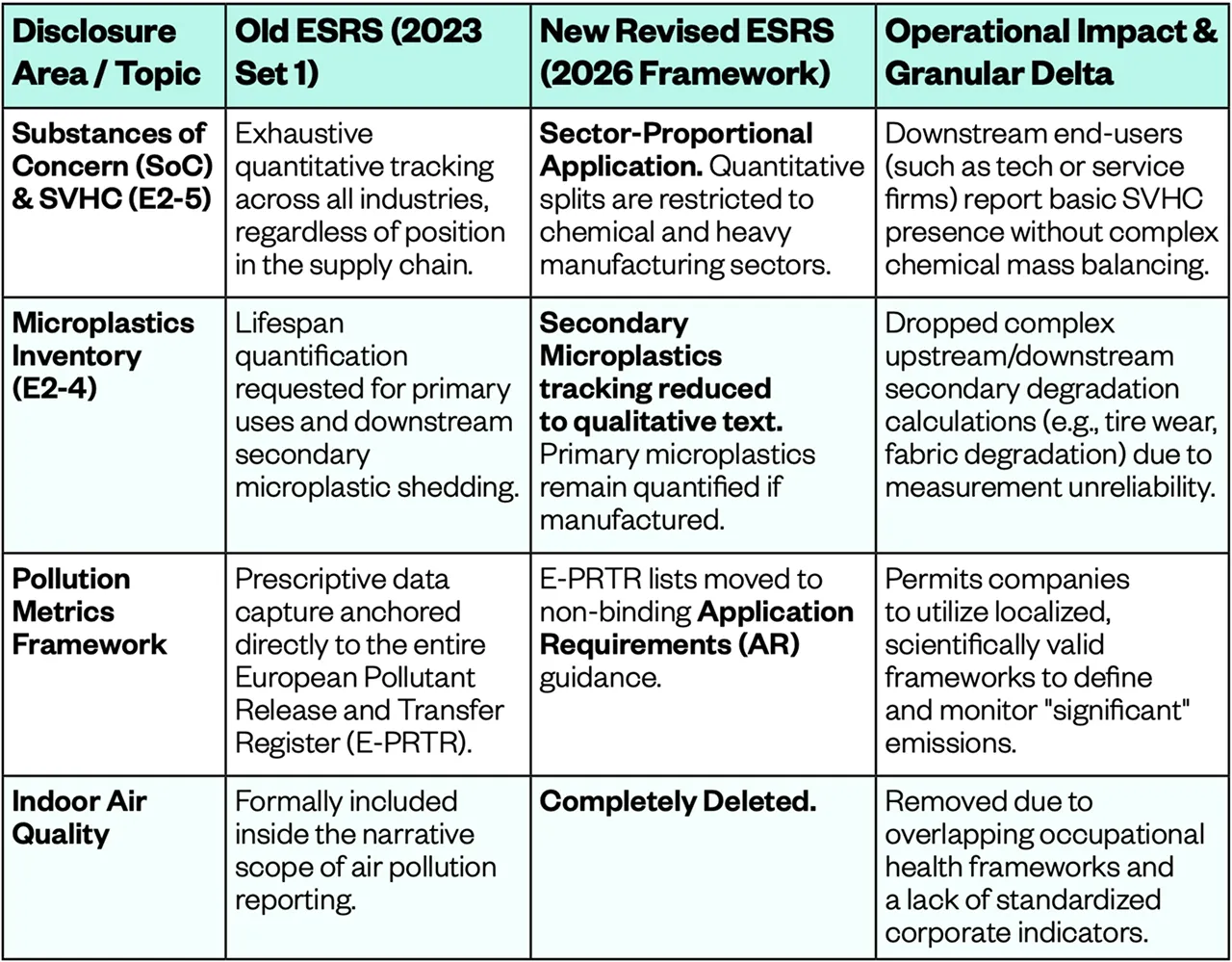

ESRS E2: Pollution

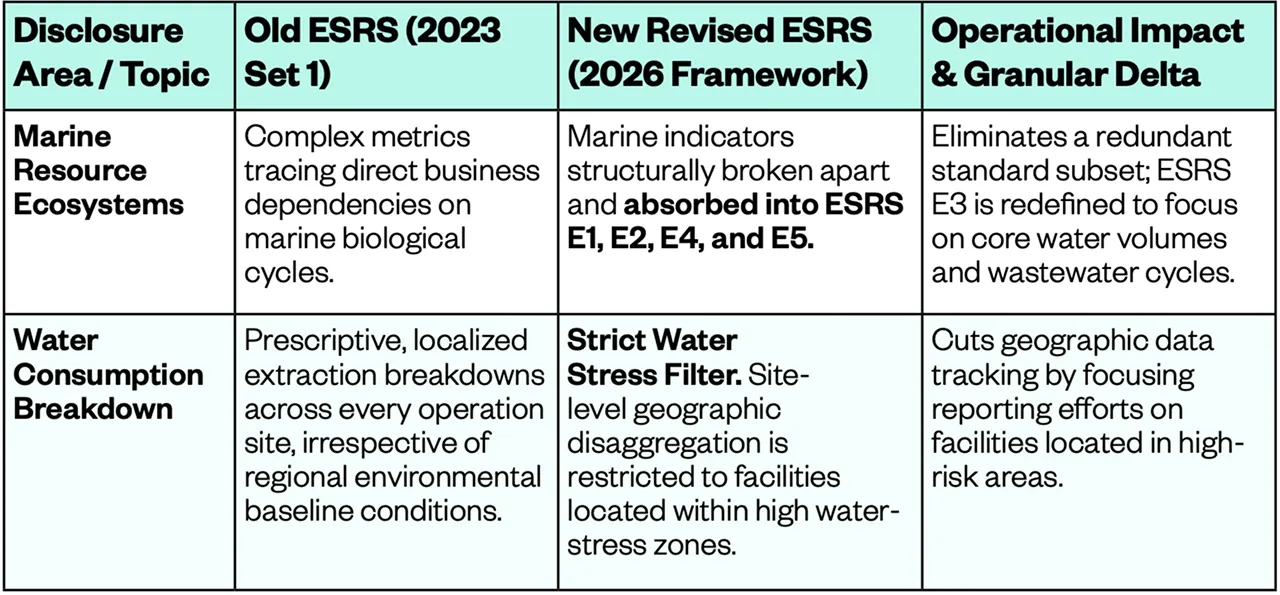

ESRS E3: Water and Marine Resources

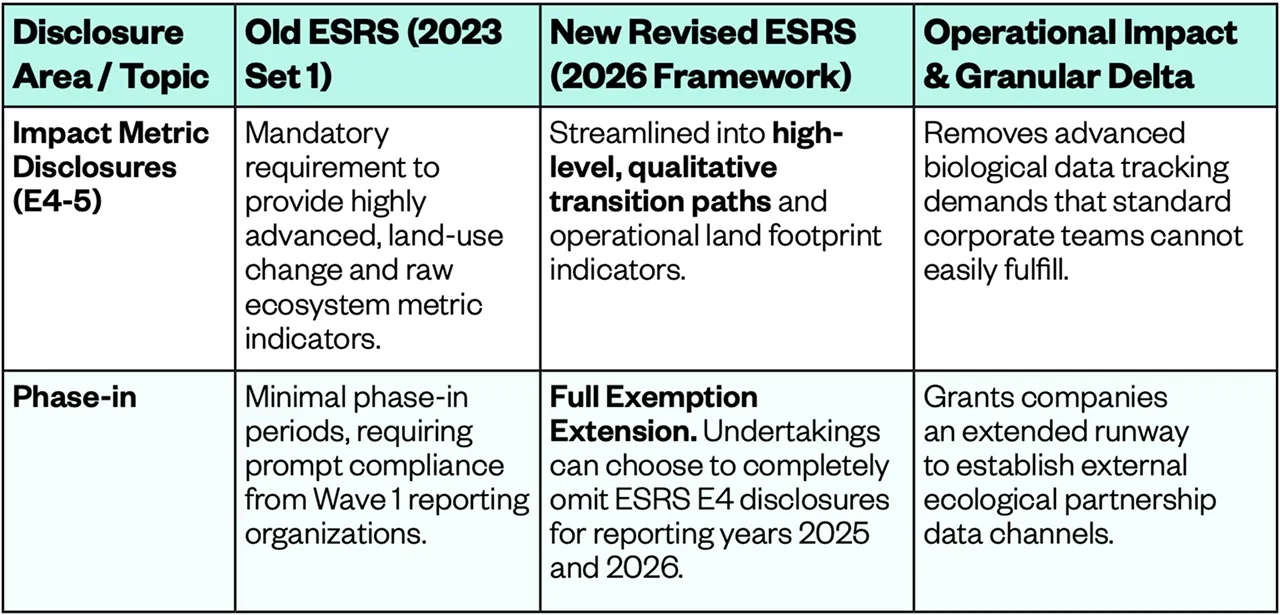

ESRS E4: Biodiversity and Ecosystems

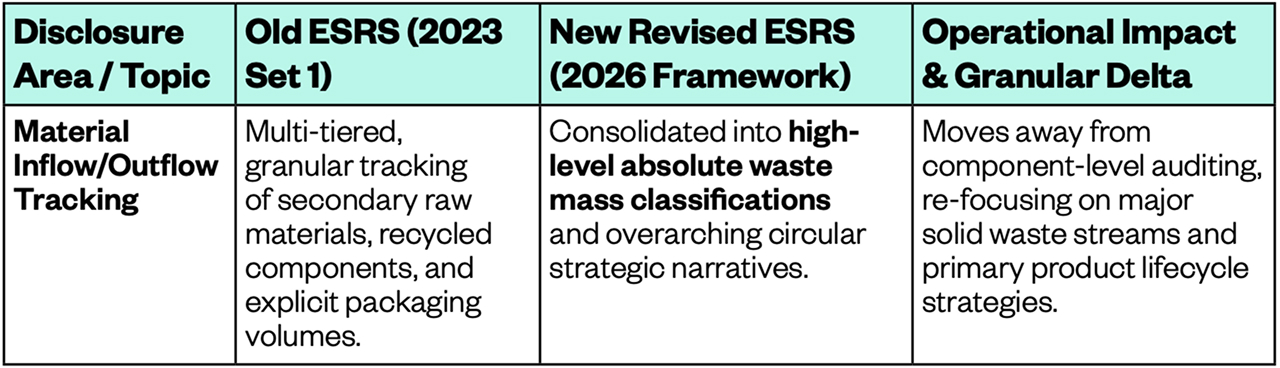

ESRS E5: Resource Use and Circular Economy

Financial Interoperability & Relief Mechanisms

Anticipated Financial Effects (AFEs across E1 to E5)

Social Standards (S-Series)

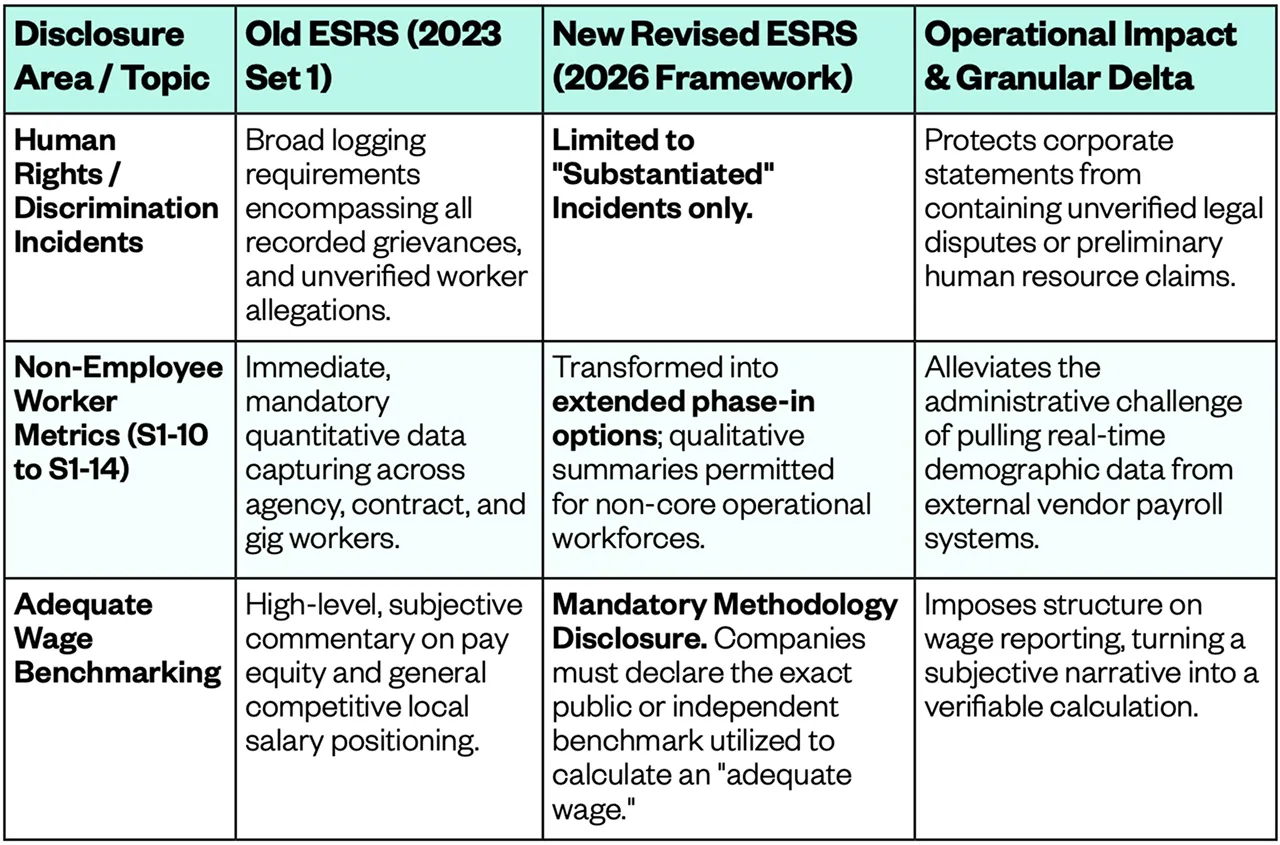

ESRS S1: Own Workforce

ESRS S2, S3, & S4: Workers in the Value Chain, Affected Communities, Consumers & End-Users

Governance Standard (G-Series)

ESRS G1: Business Conduct

Read More Articles