Policy Digest: June 2025

.avif)

INTERNATIONAL

IFRS Foundation releases education material on S2 climate-related disclosures

The new educational material provides clarity on GHG emissions-related disclosure requirements in a Q&A structure. This includes context and rationale for GHG emissions related requirements, the use of the GHG Protocol embedded in the IFRS S2 standard, and entity vs. group level emissions reporting.

In April 2025, the International Sustainability Standards Board (ISSB) released an exposure draft proposing targeted amendments to IFRS S2 climate disclosure standard. The amendments relate to GHG disclosure requirement in the IFRS S2 standard, specifically reliefs from disclosing Scope 3 category 15 emissions associated with derivatives and complex financial contracts. The proposed changes come in response to stakeholder feedback about data availability, inconsistent methodologies, and the readiness of companies to meet Scope 3 related reporting requirements. Stakeholder feedback is open until July 2025, with final rules expected by the end of 2025. Read more

IFRS Foundation releases jurisdictional profiles and snapshots outlining ISSB adoption current state-of-play

The IFRS Foundation's new jurisdictional profiles offer verified, transparent information on jurisdictions' finalized approaches to adopting or using the ISSB Standards, specifically IFRS S1 and S2, as outlined in the Inaugural Jurisdictional Guide. Jurisdictional snapshots have also been published on countries still in the consultation phase, but that have signaled intent to adopt the standards. To date, 36 jurisdictions have introduced ISSB-aligned standards. The Foundation encourages stakeholders from these jurisdictions to engage with its Regulatory Affairs team. The profiles aim to illustrate the global application of the ISSB Standards. Read more

Bank of International Settlements set to introduce framework for climate risk management

On 12 May 2025, the Basel Committee on Banking Supervision (BCBS) introduced a voluntary climate risk disclosure framework aimed at serving as a global baseline, influencing national regulators despite limited authority and resistance in the North America region. Alongside this, the Committee is assessing the Basel framework's performance during the 2023 banking turmoil, reinforcing its dual focus on financial stability and emerging climate-related risks. Read more

EUROPE

EBA proposes changes to Pillar 3 disclosure requirements

On 22 May 2025, the European Banking Authority (EBA) launched a consultation on proposed amendments to the Pillar 3 disclosure framework as part of the broader Omnibus Simplification Package, with a focus on proportionality of burden, clarity, and alignment with EU Taxonomy. Starting from end-2026, ESG disclosure requirements will be extended to large non-listed institutions, large subsidiaries of existing reporting institutions, as well as small and non-complex institutions (SNCIs), with full implementation targeted for 2027.

To ensure proportionality, the institutions will follow tailored disclosure templates based on their size and complexity. SNCIs will be required to report only essential ESG metrics—such as exposures to the fossil fuel sector—thereby reducing the reporting burden and incentivizing disclosure. While no additional disclosure obligations will be introduced for large listed banks at this stage, the EBA aims to provide enhanced Q&A documents and clarified guidance to support the practical application and interpretation of existing standards.

The revised framework (specifically templates 7,8 and 10) will be updated to cover all six environmental objectives and automatically reflect future regulatory updates. Public consultation remains open until August 2025. GAR-related templates (6–8) and Template 9 will be temporarily suspended for all institutions, including large listed banks, pending further regulatory clarification. Despite the suspension, large listed banks must continue reporting on key templates to maintain transparency during the transition, with the EBA expected to finalize the new disclosure requirements by the end of 2025. Overall, these reforms reflect the EBA’s ongoing efforts to streamline ESG disclosures, ensure alignment with the evolving EU regulatory landscape, and provide meaningful transitional support to institutions of all sizes. Read more

European Banking Authority launches ESG Dashboard to enhance access to climate risk indicators in the banking sector.

The new ESG dashboard serves as a comprehensive risk monitoring framework and tool for the assessment of transition and physical risks across the banking sector in the EU. Information is compiled from Pillar 3 disclosures and provides centralized access to climate risk indicators. The data shows that most EU/EEA banks (over 70% in most countries) have substantial exposure to counterparties contributing to climate change. This may be because of policy changes or the need to adapt with technological advancement, as well as shifting consumer preferences. While physical risk indicators are also available, the granularity of disclosed data varies based on geographical location. Additionally, methodologies for the assessment of physical risk vary across institutions.

The EBA's dashboard includes indicators for exposures secured by immovable property collateral, specifically relating to energy efficiency levels for real estate lending, as well as the Green Asset Ratio (GAR) indicator to illustrate EU/EEA banks’ alignment to EU Taxonomy criteria. Read more

NORTH AMERICA

Canada finalizes guidelines on environmental claims

The Competition Bureau of Canada has issued new guidance to help companies comply with the country’s anti-greenwashing laws passed last year. Businesses making environmental claims must back them with a credible, verifiable plan that includes interim targets. The guidelines stress the need for “actual testing” rather than anecdotal evidence or case studies. To support their claims—including net zero goals—companies must use internationally recognized, standardized methodologies and obtain third-party scientific verification. Non-compliance could result in penalties ranging from $10 million to $15 million, up to three times the revenue generated from misleading claims, or 3% of annual revenue. Read more

SEC approves application for first US sustainability exchange

On 14 April 2025, the SEC approved the Green Impact Exchange (GIX) Form 1 application, moving it one step closer to becoming the first national green stock exchange. GIX will offer dual listings for companies already listed on other national exchanges and serve as a trading venue for U.S.-registered securities. To list on GIX, public companies must adopt its sustainability standards, which emphasize strong corporate governance and climate-aligned business models aimed at delivering long-term value to investors. With the application now approved, GIX is expected to launch trading in early 2026. Read more

US DOL set to rescind ESG fiduciary rule

The Department of Labor (DOL) will no longer apply a 2022 rule which allowed fiduciaries regulated under the Employee Retirement Income Security Act (ERISA) to consider ESG and climate factors when selecting investments. Although the rule did not reference or explicitly endorse ESG investing, it upheld the legitimacy of ERISA fiduciaries presenting an ESG-focused menu of investment options. The DOL rule was challenged by 26 states in the Fifth Circuit Court of Appeals. By law, fiduciaries are bound by duties of loyalty and prudence and cannot subordinate the interests of plan participants. Therefore, all investing must be backed by sound financial analysis that considers risk-return factors. The DOL is expected to issue a new proposed rule before finalizing the new rule. Read more

US SEC announces roundtable on executive compensation disclosure requirements

The Commission is reviewing the current tabular executive compensation disclosure requirements, which have been raised as overly complex and lengthy. In addition, the use of peer benchmarking and graphical representations is under consideration to enhance clarity and usability for investors. As part of this review, the Commission is amending certain disclosure requirements based on public feedback. A roundtable will be held on 26 June 2025 to discuss these issues in depth. Stakeholders—including company representatives, investors, and subject matter experts—are invited to participate in person.

The Commission also encourages the submission of public comments online. Topics for discussion may include the process for developing executive compensation packages, efficacy of existing disclosure requirements, how to ensure that disclosures provide material, and decision-useful information to investors. This initiative follows the recent adoption of rules implementing Dodd-Frank provisions on pay-versus-performance and claw backs. Now that companies have had time to implement these rules, the Commission is also seeking input on any lessons learned during this process. Read more

CARB finalizes statutory deadlines for climate disclosure laws; delays on implementing laws

On 29 May 2025, the CARB reaffirmed the statutory deadlines for corporate climate disclosures under SB 253 and SB 261 but delayed issuing regulations that clarify which companies are in scope, creating continued uncertainty. The broad definition of “doing business in California” may include companies with minimal physical presence—such as one remote employee—if they meet state sales, property, or payroll thresholds. Draft definitions suggest “total annual revenues” will align with gross receipts (i.e., worldwide revenue), and “corporate relationships” will follow CARB’s Cap-and-Trade rules (50%+ ownership or control), though how these apply under SB 253/261 remains unclear.

CARB now expects to issue SB 253 regulations by the end of 2025 (not the previously expected 1 July 2025), while SB 261 may only receive guidance. Despite the delay, deadlines remain firm: SB 253 Scope 1 and 2 disclosures are due in 2026 (for FY 2025), Scope 3 in 2027 (for FY 2026), and SB 261 climate risk disclosures by January 1, 2026. Per a December 2024 notice, no penalties will be imposed in 2026 for incomplete SB 253 reports if companies show good faith efforts and retain relevant data. CARB continues to seek public input, explore alignment with EU and global frameworks, and plans additional workshops in 2025. Companies are advised to begin preparing using CARB’s proposed definitions. Read more

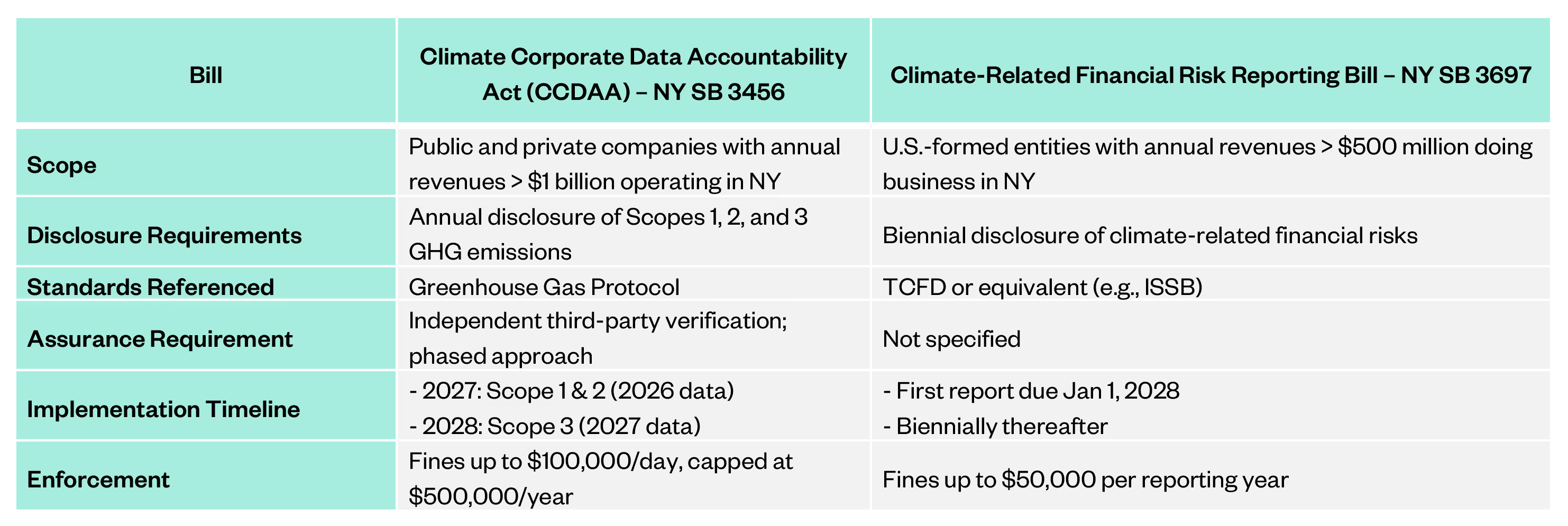

NY reintroduces climate reporting bills

New York’s Senate Bills 3456 and 3697 mandate the disclosure of greenhouse gas emissions and climate-related financial risks, respectively, closely mirroring California’s Corporate Climate Accountability Package (SB 253 and SB 261). Key requirements for both bills are outlined below:

Despite federal pushback on ESG legislation, state-level initiatives are driving progress by encouraging private companies to adopt climate reporting best practices and align with international standards such as the ESRS, TCFD, and ISSB.

ASIA-PACIFIC

Thailand Taxonomy begins Phase 2 rollout

The Thailand Taxonomy Board launched Phase 2 of the Thailand Taxonomy which extends its scope to four high impact sectors: manufacturing, agriculture, waste management, and construction. It will provide a framework for businesses to align with climate change mitigation goals. This phase, which builds on Phase I's focus on energy and transportation, will include criteria for reducing greenhouse gas emissions. This phase aims to refine the criteria for green activities, supporting the alignment of Thailand’s financial sector with environmental sustainability goals. Read more

Other News & Resources

- India’s SEBI rolls out framework for the labelling of social, sustainability or SLBs. Read more

- RIAA releases Investor Toolkit: Human Rights in Global Value Chains. Read more

Stay updated on latest regulatory developments.