Know Your Holdings: Analyzing the Hidden Patterns of Defence Sector Exposure

Key Insights

- Geopolitical tensions are reshaping national security priorities and paving the path for defence and weapons exposure in ESG-related portfolios.

- In our analysis, we find that over 500 of the 28,000+ companies screened carry defence or weapons flags.

- We find defence and weapons-related exposure in financial services and real estate — sectors not commonly associated with defence risk.

- We observe that ESG-branded ETFs, such as the iShares ESG Aware MSCI USA ETF, have as much as 13.5% of their holdings in companies with defence or weapons flags.

Background: Defence Related Activities and ESG Investments

The rising geopolitical tensions and national security concerns, from the war on Ukraine to the conflict in the Middle East, have brought defence related investments to the forefront of political and strategic discussions, and increasingly on the radar of institutional investors. According to the UN1, global military spending reached a record $2.7 trillion in 2024, marking a 9% jump from the previous year. This surge is driven not only by security imperatives, but also by a growing public narrative that frames defence spending as integral to the protection of human rights and sovereignty.

As defence spending rises globally, questions emerge on its compatibility with ESG frameworks and the exposure of institutional investors to the sector. Traditionally, companies involved in defence-related activities have been excluded from ESG-focused portfolios due to their ethical concerns and high-risk profile. However, this is changing — governments are actively developing pathways to accommodate such activities within the scope of sustainable investments.

In 2025, the European Union presented the ReArm Europe Plan/Readiness 20302 aiming to mobilise up to EUR 800 billion in additional defence spending, of which only €150 billion constitutes direct EU funding in the form of loans, with the remainder contingent on national government budgets and mobilisation of private capital3. To encourage capital flows to the defence industry, the commission clarified that investments in defence-related activities are compatible with the EU sustainable finance framework, including the Sustainable Finance Disclosure Regulations (SFDR). It encouraged assessment of these activities on a case-by-case approach. Additionally, Germany has approved a €52 billion military expenditure package4 with aims to reach NATO’s enhanced 3.5% GDP defence spending commitment by 2029. While the United Kingdom’s 2025 Strategic Defence Review5 has set a target of allocating 2.5% of GDP to defence by 2027 and called for the development of new funding frameworks that would make defence-focused innovators more appealing to private sector investors. Across the Atlantic, the United States of America has proposed a massive $1.5 trillion defence budget for the fiscal year 2027, marking a 42% increase over current funding levels.

While the trajectory is clear, it bears noting that defence-related activities present considerable investment risks. These investments are assessed differently across sustainable finance frameworks and depend on the nature of involvement of the companies. Understanding these classifications is therefore central to how institutional investors and financial institutions assess and engage with the sector.

Drawing the Line: How ESG Frameworks Classify Defence-related Activities

There is no standard approach for the assessment and classification of defence-related activities. Each framework, whether regulatory or developed by rating providers, differs in its methodologies and assessment criteria for screening these activities. The assessment generally covers the company’s business activities, the degree to which its products or services contribute to conventional or controversial weapons, and whether that involvement is direct or indirect through corporate ownership structures. The process follows a multi-layered process, beginning with absolute exclusions grounded in activity type and transitioning to quantitative thresholds based on financial materiality.

The assessment process begins with the application of an exclusionary screen, targeting companies that contribute to controversial weapons. These activities carry serious social and reputational risks and are considered incompatible with sustainable investment mandates. For example, companies that derive revenues from controversial weapons cannot be included in EU Paris-aligned benchmarks and Climate Transition Benchmarks, nor would they be eligible for inclusion in portfolios of products tracking those benchmarks.

While there is no universally agreed definition for controversial weapons, these exclusions are grounded in ratified international conventions and treaties. In the case of the EU, these include:

- Convention on Cluster Munitions 2008

- Ottawa Convention 1997

- Biological Weapons Convention 1972

- Convention on the Prohibition of Chemical Weapons 1993

Together, these international conventions place anti-personnel mines, biological and chemical weapons, and cluster munitions under the controversial weapons category. However, fund managers and ESG rating providers go beyond to include depleted uranium, incendiary weapons, and nuclear weapons in their frameworks. Beyond involvement in controversial weapons, companies are also screened against the UN Global Compact principles and OECD Guidelines for Multinational Enterprises for involvement in any controversies. Any severe controversy, including human rights violations or involvement in illegal defence activities, results in the exclusion of the company from sustainable investment portfolios, regardless of its revenue exposure.

After the exclusionary screen, the process shifts to revenue and ownership screens to assess companies involved in conventional defence activities. Regulatory frameworks and rating providers apply direct revenue thresholds, varying by framework but typically ranging from 5% to 10%, to determine the share of total turnover derived from defence-related activities. Companies that exceed these thresholds are excluded from sustainable investment portfolios. This process also covers ownership screens that map corporate structures to identify indirect involvement, ensuring that exposure through a parent company or subsidiary does not breach exclusion criteria even where the primary entity falls below the applicable revenue threshold.

While this has been the broadly adopted approach, a significant regulatory development came with the recent EU Defence Omnibus Package6, which clarified that defence sector investments are compatible with the broader sustainable finance framework provided they are not involved in weapons banned under major international agreements to which EU Member States are parties. The commission classified the weapons banned under the conventions as “Prohibited Weapons,” revising its regulatory terminology from “controversial weapons.” This classification is important as it leaves depleted uranium, incendiary weapons such as white phosphorus, and most importantly nuclear weapons outside the categorisation of prohibited weapons. This is because the Treaty on the Prohibition of Nuclear Weapons has not yet received broad ratification by states, including the EU. While these weapons have traditionally been excluded from sustainable investments, the revised classification could potentially open the door for institutional investors to enter this category. This trajectory is already reflected in fund data — according to Bloomberg7, the number of ESG equity funds with exposure to the nuclear arms industry rose by more than 50% following Russia’s invasion of Ukraine in 2022.

Against this backdrop, we conducted an analysis to understand the extent of corporate exposure to defence-related activities.

The Current Landscape – Defence Exposure in Sustainability Related Portfolios

In this analysis, we outline critical insights from recent data on corporate involvement in the defence and weapons industry. The findings reveal that exposure is more widespread and complex than commonly understood, extending into non-traditional sectors and even ESG-focused investment products. This presents significant, and often overlooked, financial, regulatory, and reputational risks for financial institutions.

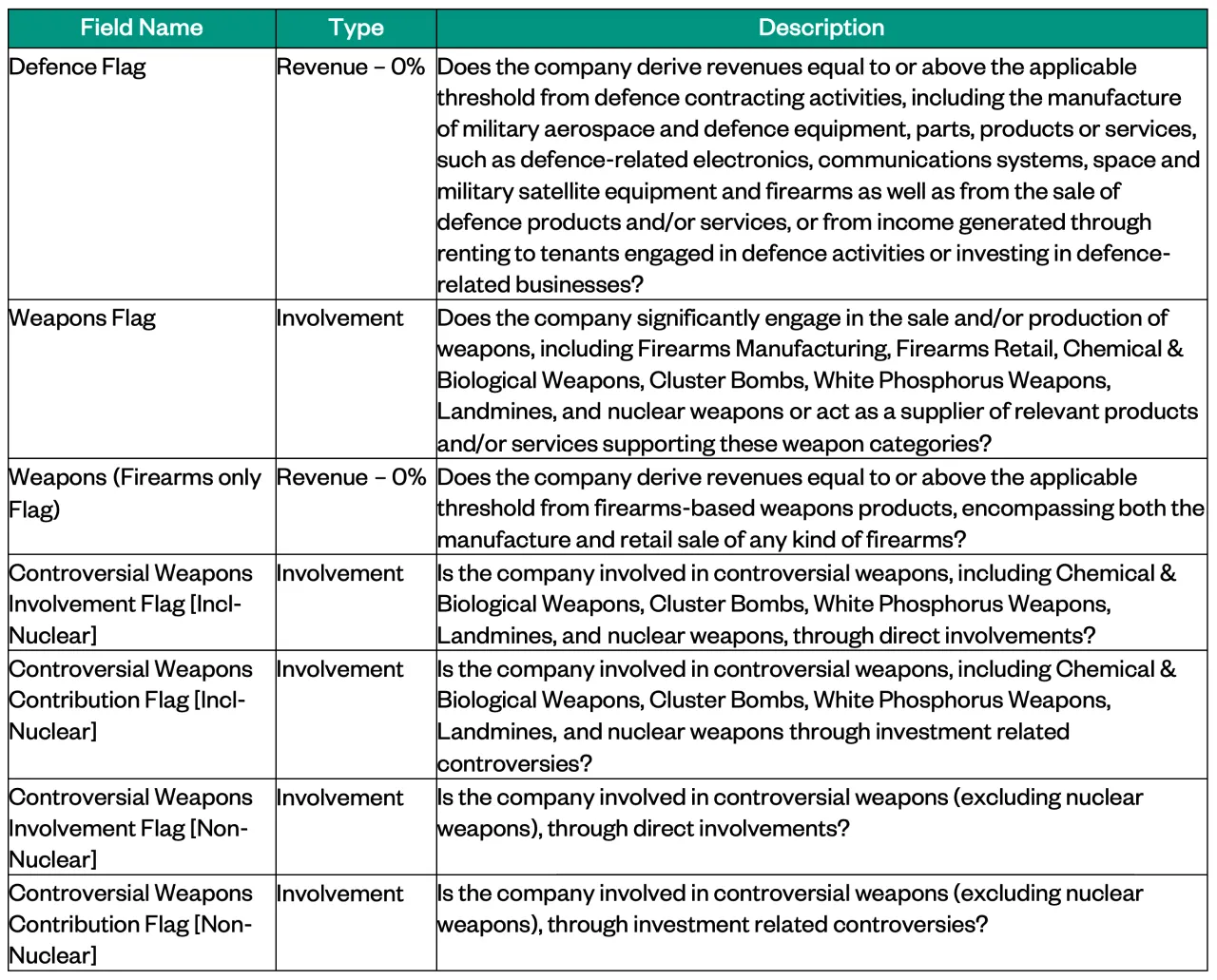

The analysis leverages ESG Book’s Business Involvement Filter, which was developed to systematically screen 28,000+ companies for revenue or business involvements and allows investors to align their values across public equity and fixed income portfolios. We use 2 different types of data depending on what is best suited for a particular filter. The revenue breakdown data tracks reported company revenue from financial statements and 10-K annual reports. Where the revenue figure for a filter is greater than 0%, the company is flagged. The business involvement data tracks products and services sold by companies as reported on company websites or in company reports and presentations. The table below represents the defence related business involvement flags:

The results are presented across four distinct areas: scale of corporate involvement in defence related activities, its exposure at the industry level, geographic concentration of such exposure, and the representation of defence linked companies within ESG-labelled funds.

I. Scale of Involvement

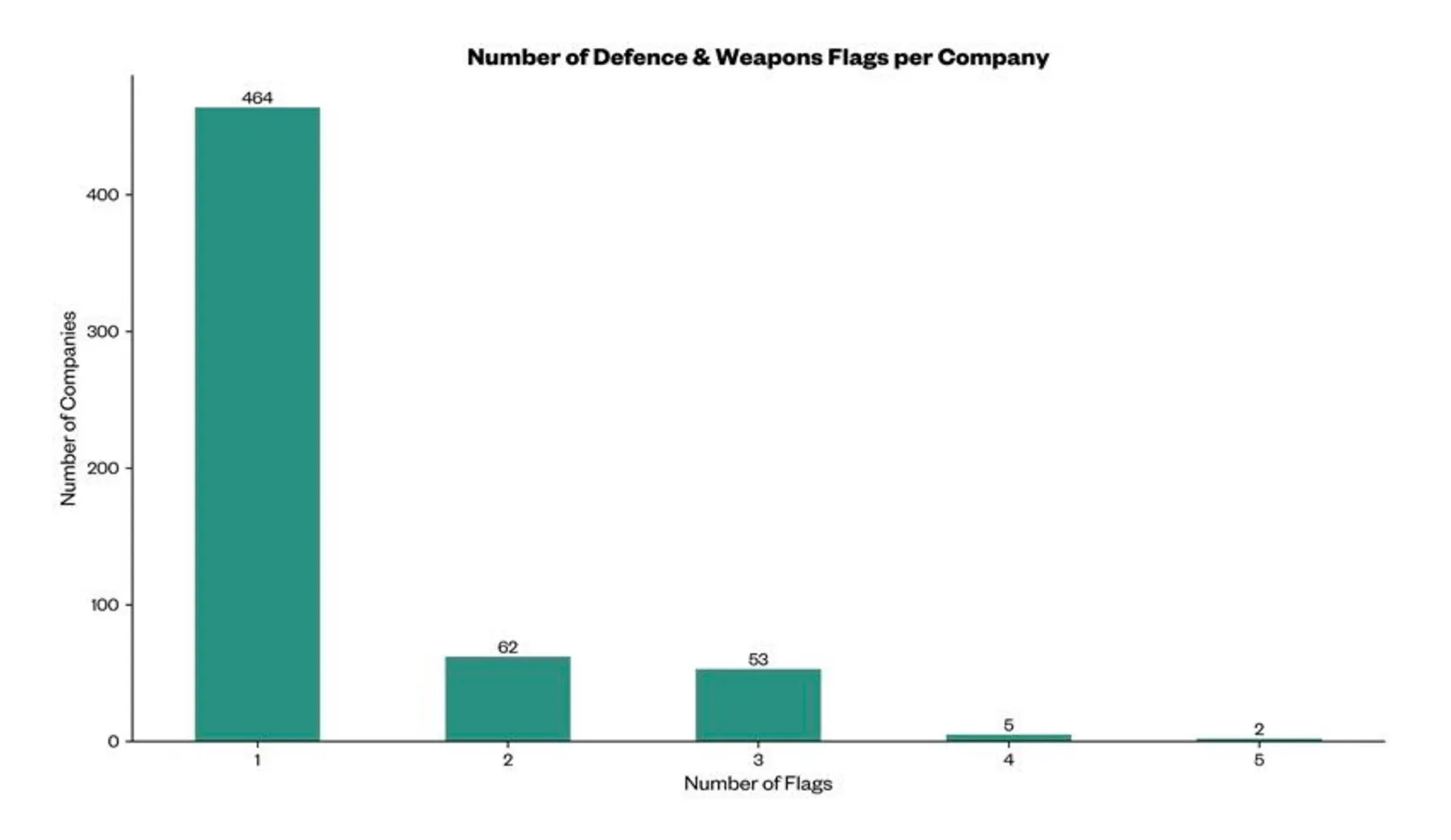

Our analysis on scale of corporate involvement suggests that over 500 companies are flagged for defence-related activities. Majority of these companies, 464 in total, carry a single flag, suggesting a focused or limited area of defence-related business. However, a notable subset holds multiple flags, reflecting more complex, diversified operations that span several areas of the sector.

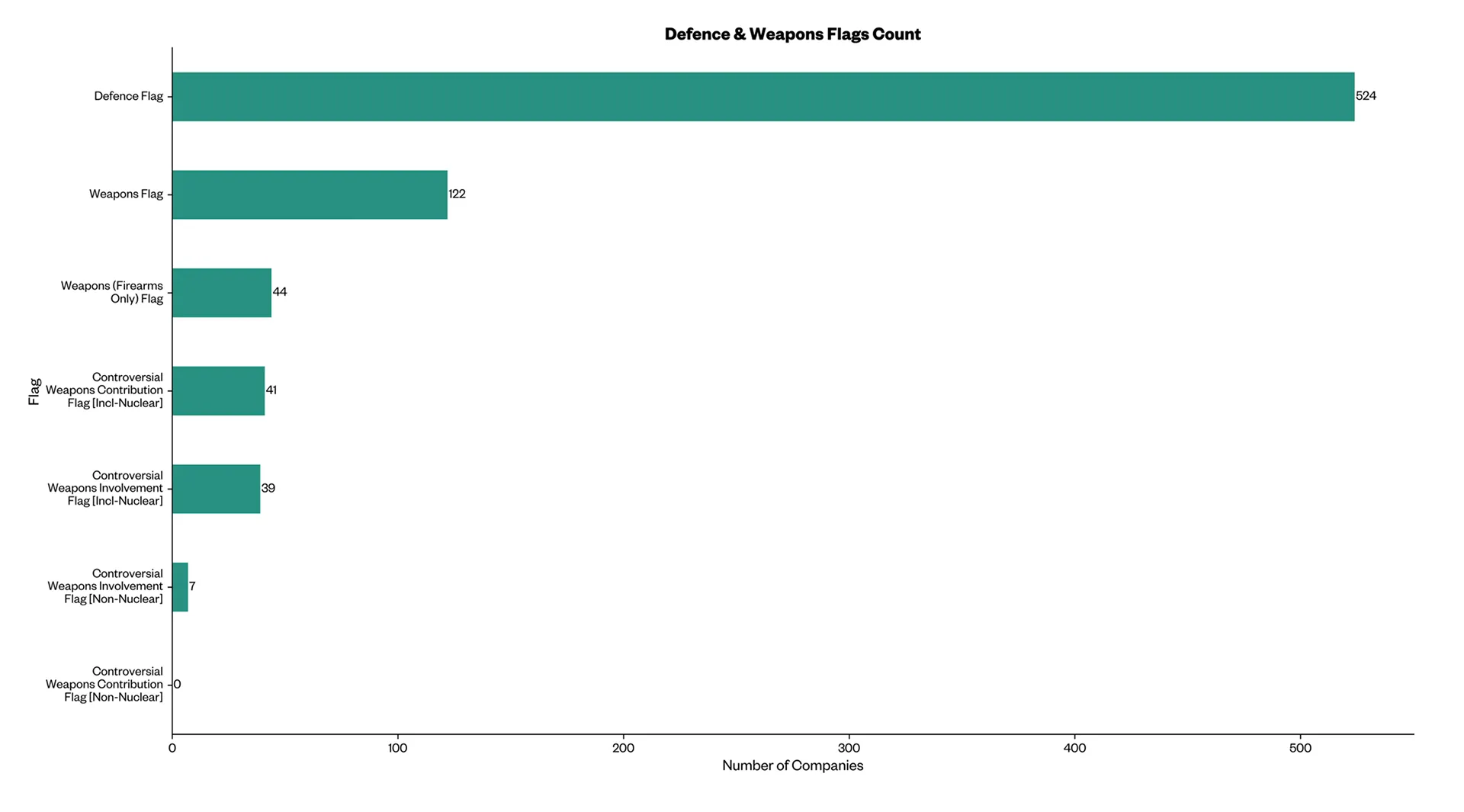

Our analysis also suggests that the majority of these 524 flags are for involvement in non-controversial defence, weapons, and firearms flags. However, 80 companies are flagged for either involvement or contribution to controversial weapons including nuclear weapons.

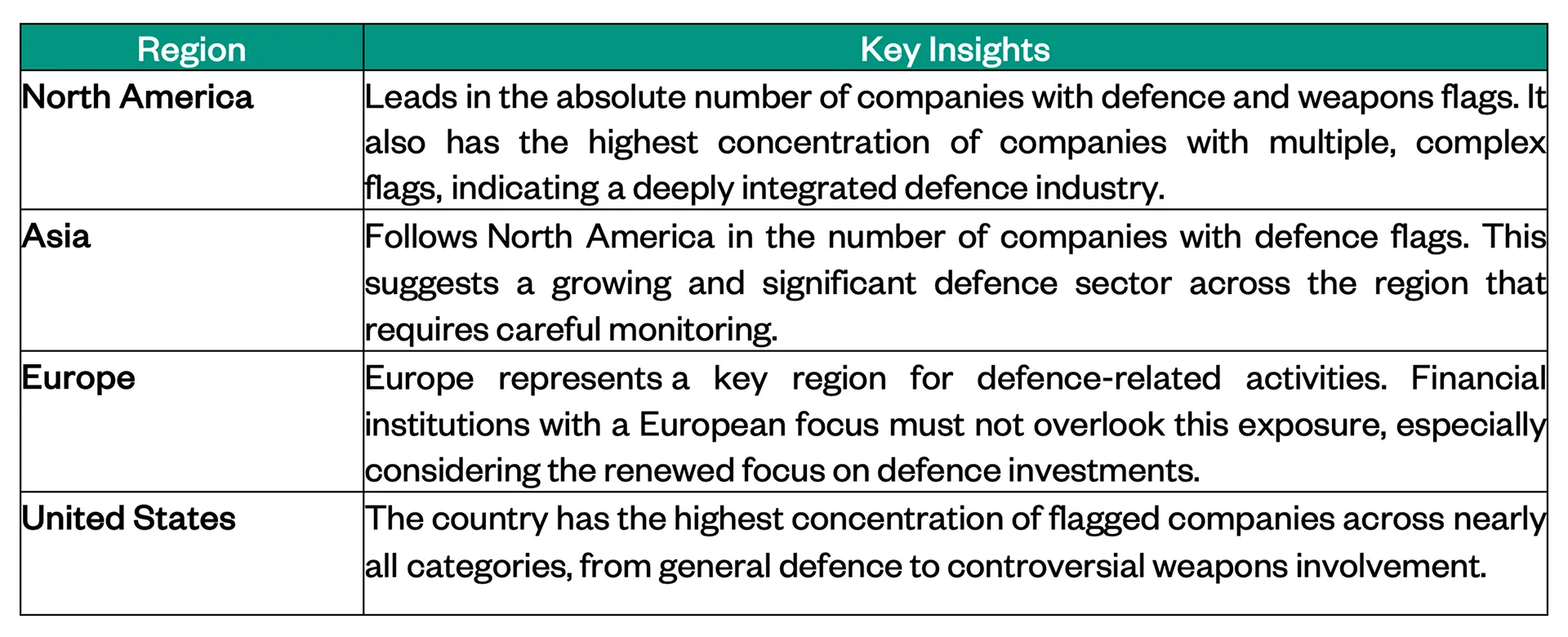

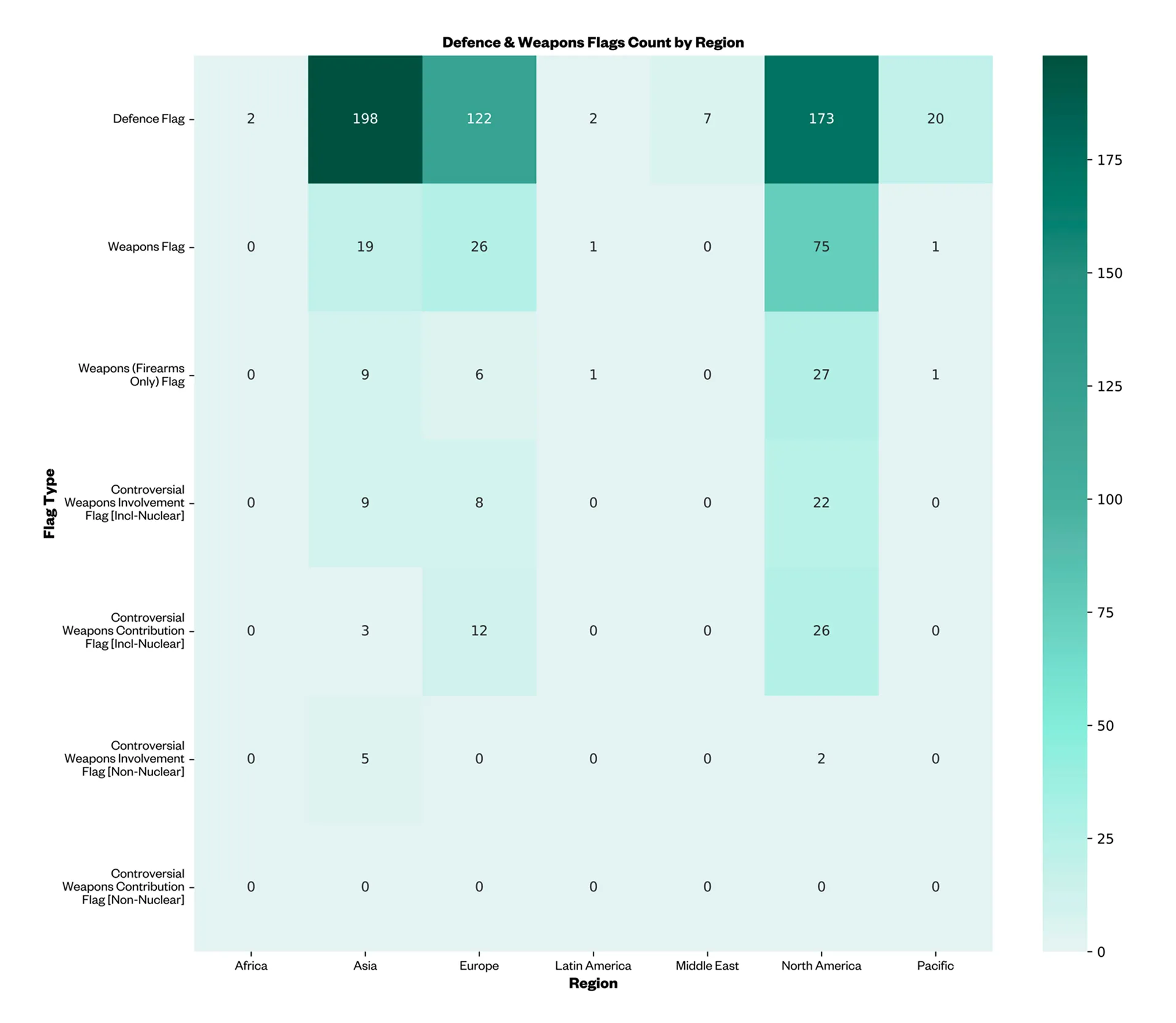

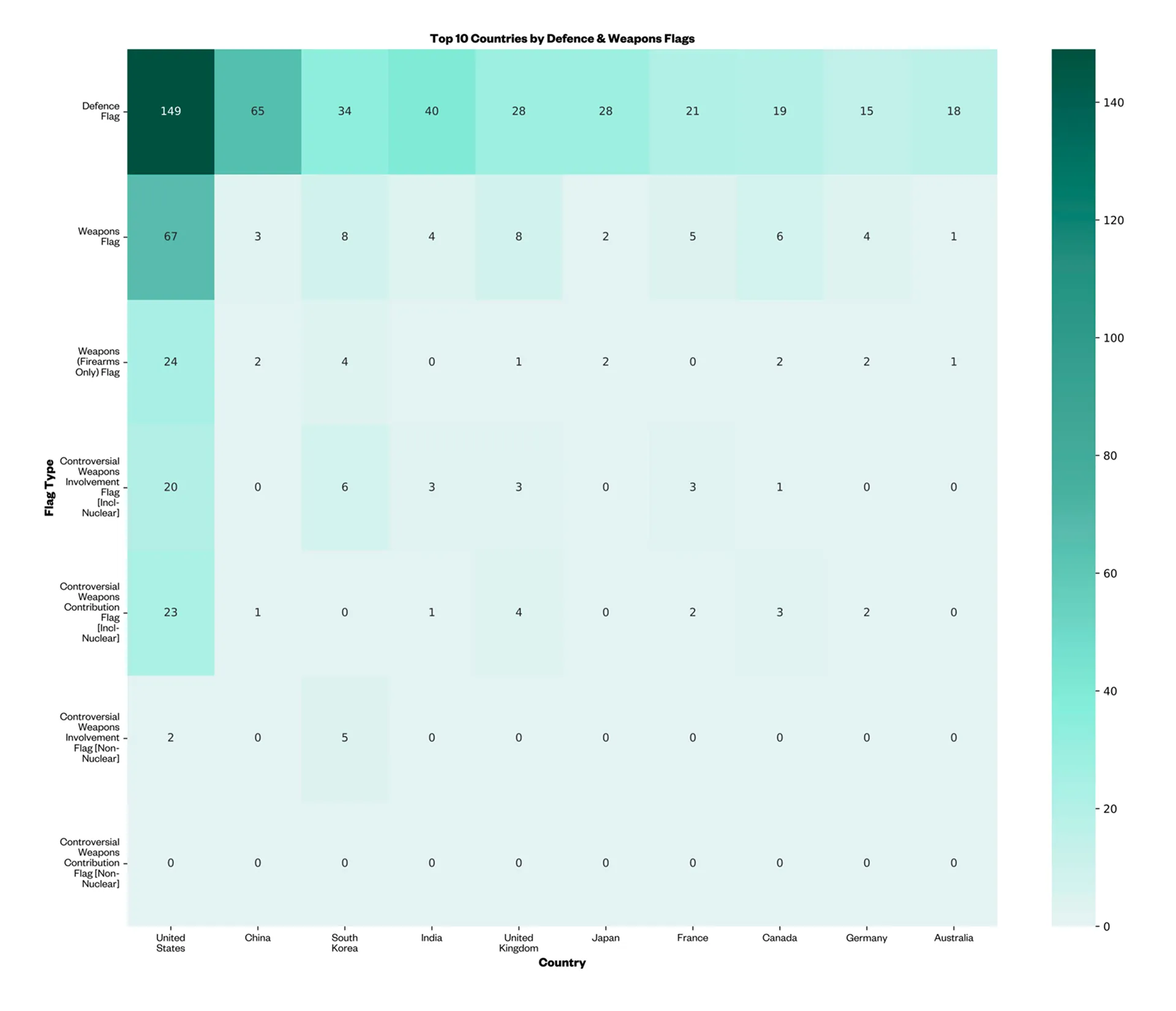

II. Geographic Concentration & Exposure

The data suggests that defence and weapons-related activities are heavily concentrated in developed economies, but the nature of this exposure varies significantly by region. We observe the following:

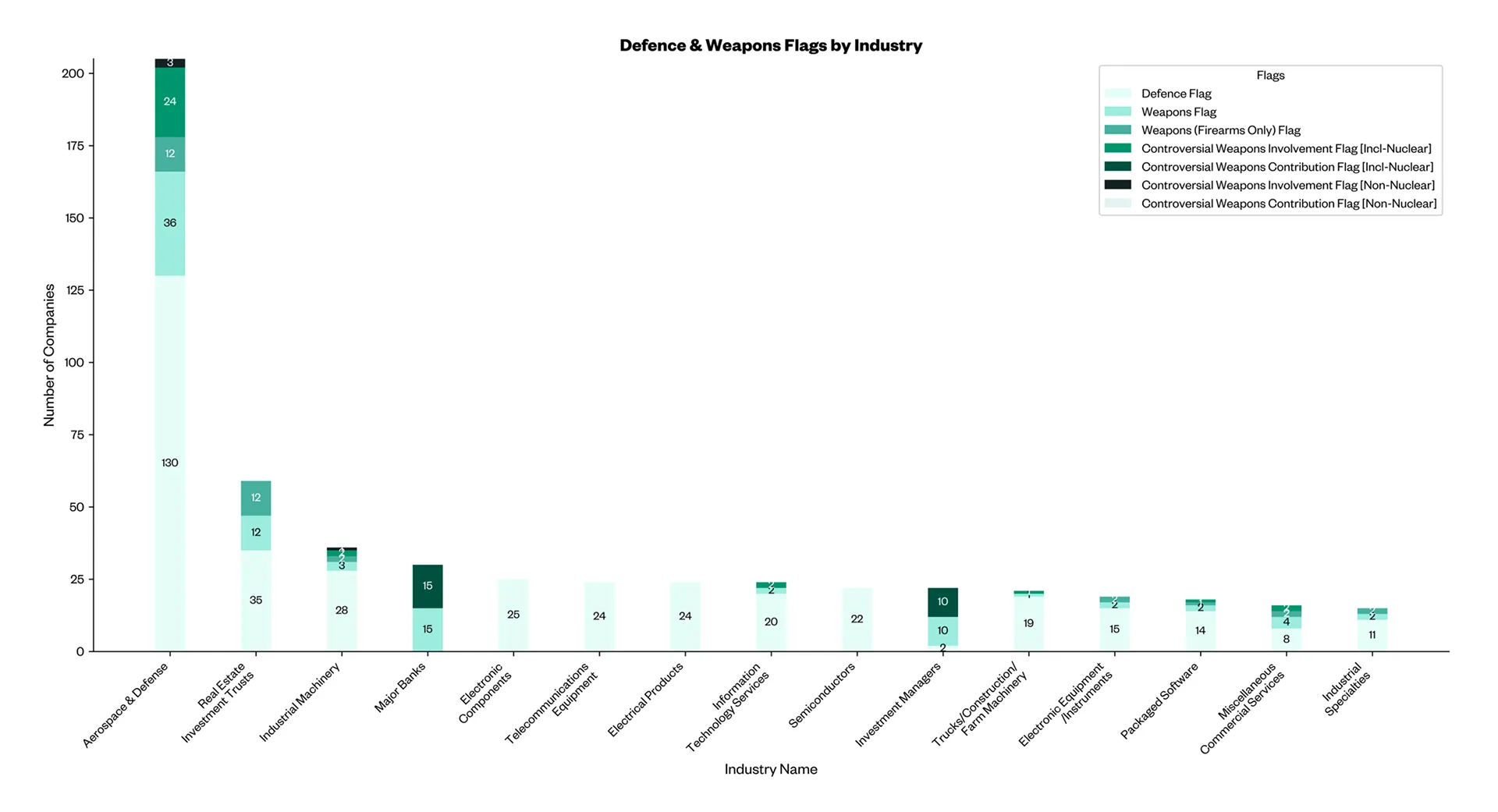

III. Analysis of Industry & Financial Exposure

In our analysis, we observe that the Aerospace & Defence sector is predictably the most exposed sector (with nearly 70% of its companies flagged) to defence and weapons flags. However, significant exposure exists in industries that may not be on a typical risk radar.

- Financial Sector Involvement: The analysis highlights Major Banks and Investment Managers as two categories with particularly notable exposure. Of these, 15 major banks and 10 investment managers have been flagged specifically for controversial weapons contribution indicating a direct financial link with companies engaged in the production or distribution of such weapons.

- Real Estate Links: Real Estate Investment Trusts (REITs) show a surprisingly high number of defence flags (35 companies). This suggests significant business relationships, such as leasing property to defence contractors or government military facilities, representing an indirect but material link to the sector.

IV. Defence and Weapons Linked Companies in ESG Labelled Funds

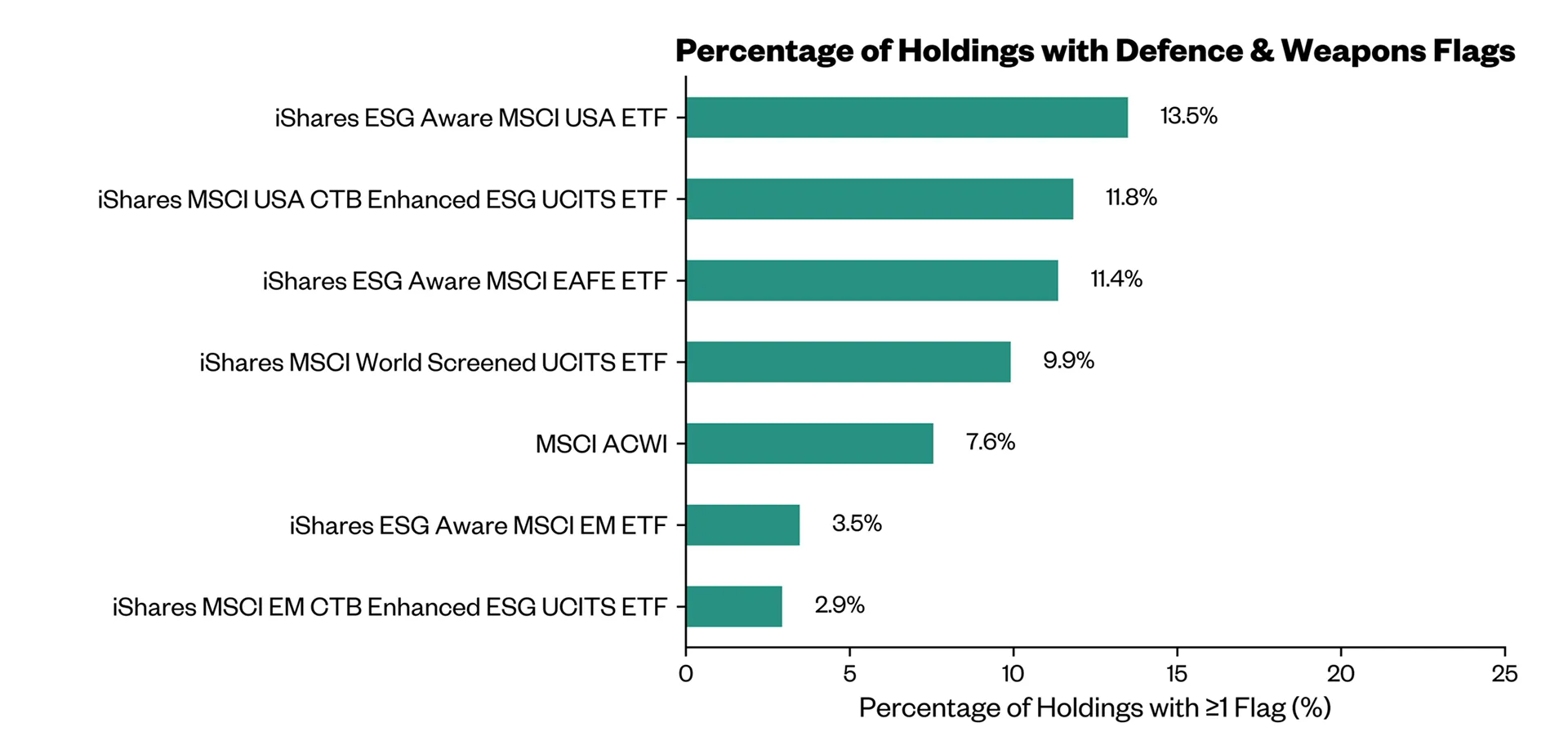

A crucial finding comes from our analysis of Blackrock’s ESG-labelled funds. We find the presence of defence and weapons-linked companies within investment funds marketed as ESG. We observe the following:

- Significant Holdings in ESG Funds: ESG-branded ETFs, such as the iShares ESG Aware MSCI USA ETF, were found to have as much as 13.5% of their holdings in companies with defence or weapons flags. Other ESG-screened and enhanced funds also showed exposure ranging from 3% to 12%.

These findings substantiate the hypothesis of defence linked companies within investment funds. It is, therefore, important to examine the ESG screening approaches as it poses serious reputational risks for institutions and their clients who depend on such labels to fulfill ethical investment commitments.

Recommendations for Financial Institutions

There is a structural shift in how European and other international policymakers view defence expenditure, not as a departure from responsible governance, but increasingly as a component of it. However, the defence industry presents significant challenges — characterised by a lack of transparency, complex supply chains, and high ESG and reputational risks for companies with links to the sector. In our analysis, we have already identified defence-related exposure within ESG-focused funds and corporate involvement distributed across sectors. These factors underscore the need for a more comprehensive and nuanced approach to risk assessment that should account for:

- Enhanced Due Diligence: Standard industry classifications are no longer sufficient to capture the full scope of defence and weapons exposure. Financial institutions should deepen their due diligence frameworks to encompass financing relationships, investment structures, supply chain dependencies, and indirect exposures such as property holdings. This includes conducting background checks on ownership structures, business operations, client profiles, and countries of operation. Lending agreements should incorporate “Indirect Financing Risk” assessments, including “Use of Proceeds” clauses, to ensure capital is not diverted toward prohibited weapon lines or sanctioned parties.

- Review ESG Policies and Screening Criteria: Internal ESG policies and screening methodologies should be reviewed in light of the evolving regulatory landscape. A granular activity-based screening approach is recommended over broad sector-based exclusions, enabling more precise identification of defence and weapons exposure across portfolios. Institutions should also monitor how major index providers and ESG data providers are updating their own frameworks in response to policy shifts.

- Proactive Risk Management: The presence of defence-related flags in non-traditional sectors such as major banks and REITs signals that risk management frameworks must be applied more broadly than conventional approaches allow. Institutions should map indirect exposures across their entire portfolio, including sectors not historically associated with defence risk.

- Transparency and Client Communication: Given that ESG-labelled funds carry exposure to defence and weapons-flagged companies, institutions face serious reputational risk. Firms should proactively communicate how their ESG screening methodologies address defence exposure, and where relevant, disclose the nature and extent of any such holdings. This is particularly important for funds marketed to clients with explicit ethical investment mandates.

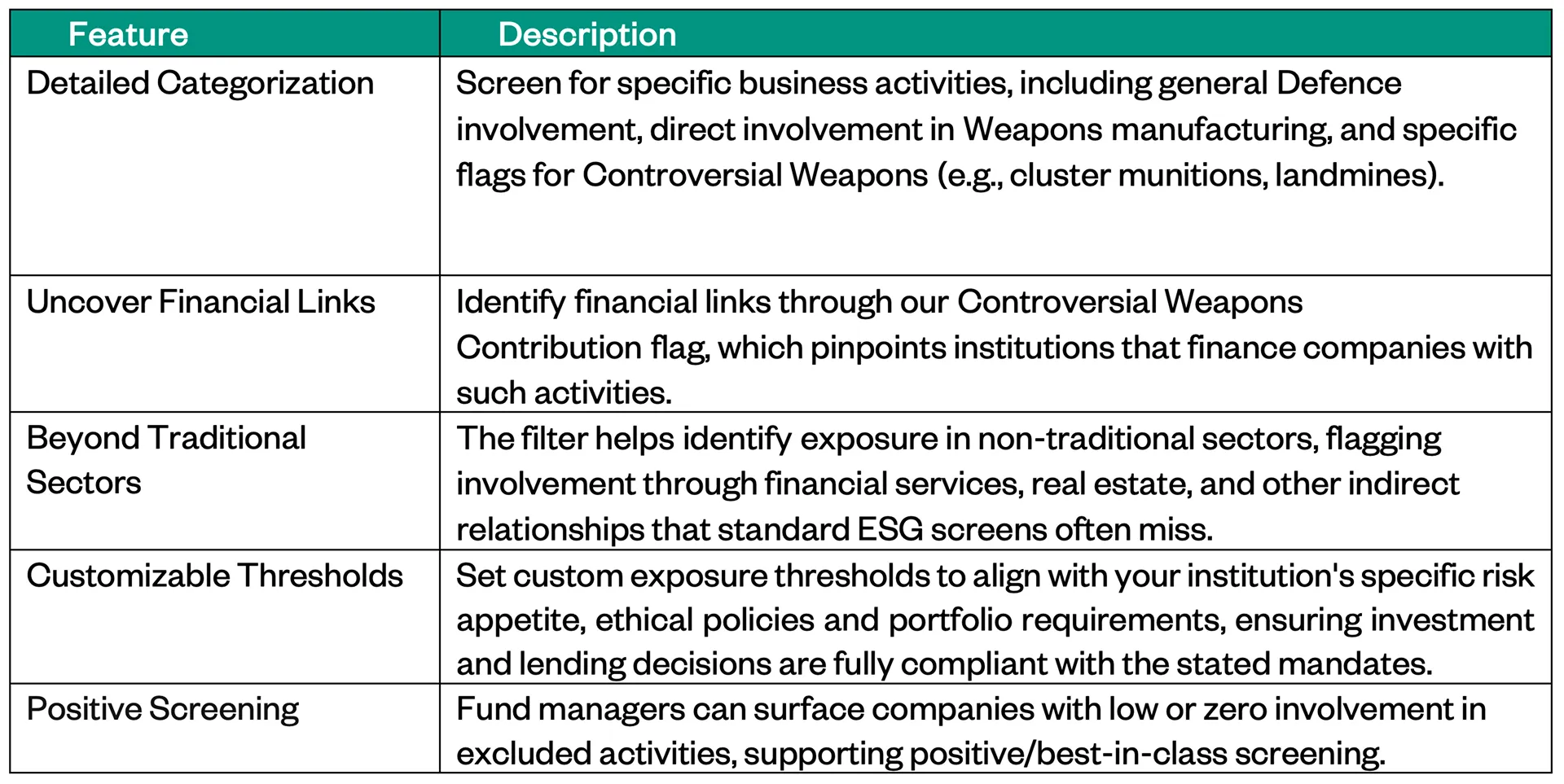

A Proactive Screening Tool to Navigate Defence Exposure – ESG Book’s Business Involvement Filter

To address these complex challenges, ESG Book offers a powerful solution: the Business Involvement Filter that covers 28,000+ companies — screens them, tracks corporate revenues, and helps mitigate risks efficiently. This tool is designed to provide granular, activity-based data that financial institutions need to navigate the hidden risks of defence and weapons exposure. Our filter moves beyond broad industry codes to provide precise screening across a spectrum of involvement types. This allows for a truly nuanced understanding of portfolio risk:

By leveraging the Business Involvement Filter, financial institutions can move from a reactive to a proactive risk management stance. This enables you to conduct more robust due diligence, prevent reputational damage, and ensure that your investment products, especially those marketed as ESG, align with client expectations and regulatory requirements.

1 https://www.un.org/en/peace-and-security/the-true-cost-of-peace

2 https://www.consilium.europa.eu/en/policies/european-defence-readiness/

3 https://commission.europa.eu/topics/defence/future-european-defence_en

4 https://www.dw.com/en/german-lawmakers-approve-billions-in-military-expenditure/a-75206445

5 https://www.gov.uk/government/publications/the-strategic-defence-review-2025

6 https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:C_202504950

7 https://www.bloomberg.com/news/features/2025-08-24/nuclear-weapon-manufacturers-tap-esg-billions