From Compliance to Strategy: ESG Book’s Take on the EBA’s Pillar 3 ESG Disclosure Standards Update

Introduction

On the journey toward a more robust and sustainable financial system, the European Banking Authority (EBA) has taken another decisive step. It recently issued a consultation on the latest set of draft Implementing Technical Standards (ITS) under Pillar 3 that sets out a broader and more granular framework for ESG disclosures. The proposals, set to apply from December 31, 2026, extend sustainability disclosure requirements beyond large, listed banks and aim to harmonise and enhance transparency across the EU banking sector.

From ESG Book’s perspective, this marks a crucial evolution in how sustainability data will be captured, structured, and disclosed across the European financial system — and presents a strategic opportunity for banks to streamline and optimise their non-financial risk management and data frameworks.

This post unpacks the EBA’s key proposals, the changes to reporting templates, what they mean for different types of institutions, and the opportunity to harness technology platforms for enhanced compliance.

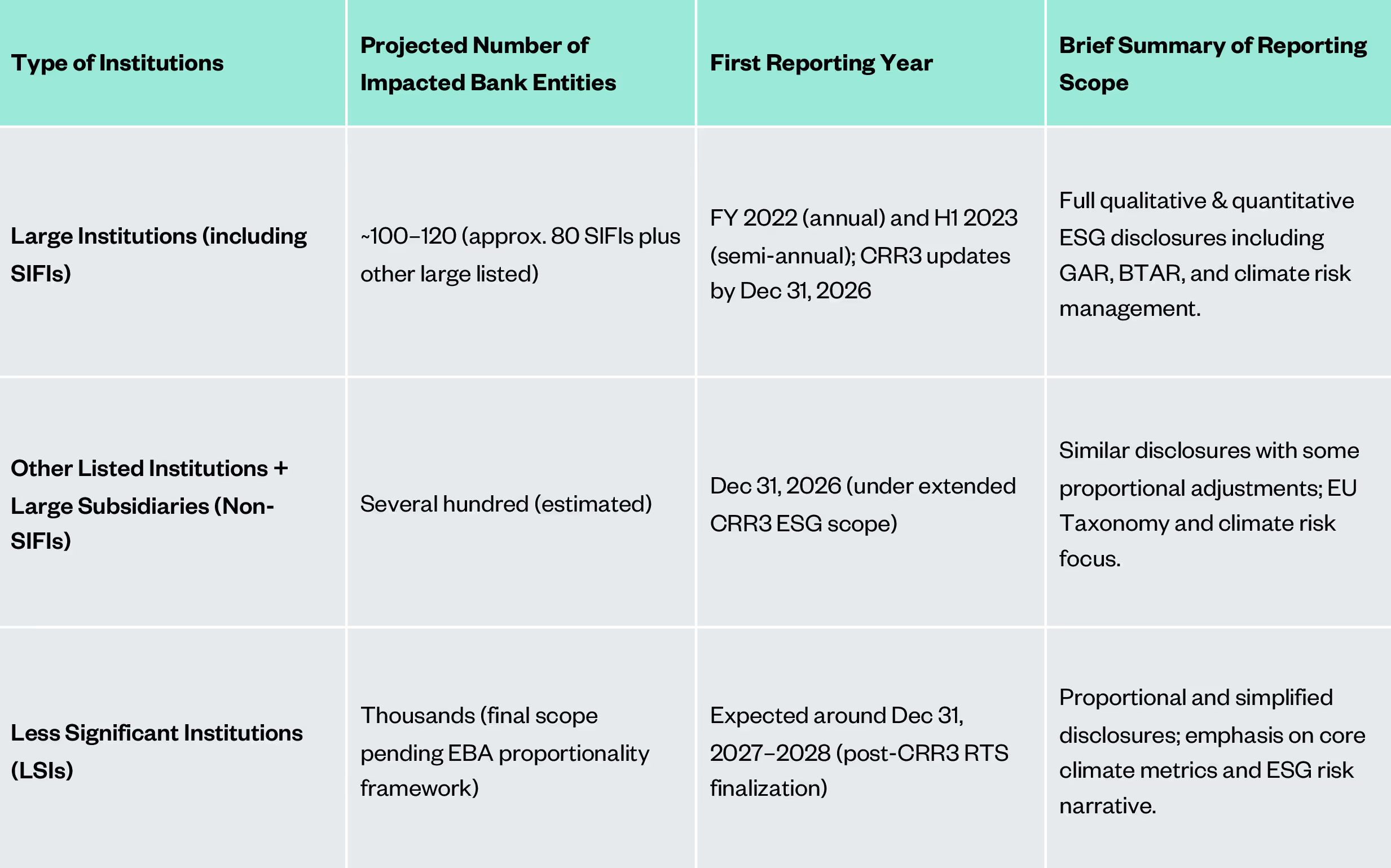

1. Expanded Disclosure Requirements: More Banks in Scope, Tailored Templates

The EBA’s new approach would apply to a broader set of financial institutions, moving beyond large listed entities and systemically important financial institutions (SIFI) to include:

- Large non-listed institutions

- Other listed institutions

- Small and non-complex institutions (SNCIs)

- Large subsidiaries

EBA Pillar 3 ESG Reporting Requirement Timelines and Scope of Obligations:

Go-Live: From 31 December 2026, with a transitional period where large listed institutions continue reporting under the existing framework (except for suspended Templates 6–10 on Green Asset Ratio and EU Taxonomy reporting).

ESG Book Insight: This tiered framework will necessitate modular data disclosure solutions. ESG Book’s platform architecture is well-positioned to support differentiated user pathways — from full, template-based ESG data mapping for large banks, to lean, essential modules for SNCIs and subsidiaries.

2. Template Revisions: More Granular, Forward-Looking Disclosures

The draft ITS introduces major updates to the structure and scope of disclosure templates, including:

New Sector Classifications (Template 1 & 1A)

- Updated to NACE Rev. 2.1

- More granular coverage of fossil fuels and agriculture

- Inclusion of Scope 1 and 2 GHG emissions, and new metrics on proxy data usage (per PCAF methodology)

ESG Book Insight: The enhanced sector granularity and proxy tracking align closely with ESG Book’s capabilities in data mapping and emissions estimation.

Template 2 – Real Estate

- Adds new fields for covered bonds and energy performance data (including proxy-estimated energy performance certificates (EPC) labels)

- Clarifies structure and use of estimates

Template 3 – Alignment Metrics

- New focus on GHG intensity-based targets

- Requires disclosures for baseline year, 2030 targets, and any post-2030 goals

ESG Book Insight: The shift toward forward-looking, intensity-based alignment enables ESG Book to harness both its existing data capabilities on climate analytics and its disclosure utility platform for more tailored and granular reporting by counterparties.

Template 5 – More Specific Physical Risk Disclosures

The chronic/acute physical risk split is now replaced by four distinct climate hazards (related to temperature, wind, water, solid mass), better aligned with climate science and EU regulations. Institutions must also disclose exposure to the top 10 NUTS (Nomenclature of territorial units for statistics) regions and provide methodological transparency.

ESG Book Insight: The proposed updates related to physical risk exposures signal a clear push toward data-driven, geo-tagged exposure analysis. To meet the enhanced requirements, banks would require dedicated risk mapping and spatial data toolkits that support regional granularity, hazard tagging, and enhanced scenario visibility for physical risks.

Taxonomy Templates (6–10): Clarified but Delayed

While Templates 6–10 are suspended until end-2026, reporting on banks’ Taxonomy-aligned exposures comes back with key changes:

- Must now cover all six environmental objectives

- Streamlined disclosures projected to reduce required datapoints by ~89%

- Introduce a 10% de-materiality threshold in line with Omnibus proposals.

Additionally:

- Non-CSRD corporates are removed from the GAR denominator

- GAR and BTAR templates are harmonized with the Taxonomy Regulation

ESG Book Insight: The clarified scope of GAR & BTAR reporting would enable banks to better present their sustainable financing activities by focusing on in-scope assets. Moreover, the suspension of these templates for more than a year does not mean that financial institutions necessarily need to cease EU Taxonomy data efforts. The full inclusion of all six environmental objectives requires even greater Taxonomy data capabilities post-2026.

3. Governance and Methodology Disclosure: More Transparency, More Change Tracking

Regarding the qualitative, strategy-focused EBA Pillar 3 disclosures, the updates to Table 1 now demand greater detail on internal governance structures, methodology updates, and change tracking year-on-year.

ESG Book Insight: These shifts emphasise auditability and historical data integrity. By harnessing ESG Book’s transparency-based platform, access to source documentation and full score input traceability, banks can track and explain evolving methodologies directly on the platform.

Conclusion: A Deliberate Step Toward Better ESG Risk Management

The EBA's new Pillar 3 proposals represent a deliberate, structured move toward greater ESG transparency across the EU banking system. While not without complexity or uncertainty, they reflect a maturing regulatory landscape that is increasingly aligning financial stability with sustainability goals.

Next Steps for Banks:

- Begin internal alignment with NACE Rev. 2.1 sectors

- Review governance structures and data methodologies

- Engage in the public consultation (open through 22 August 2025)

- Prepare infrastructure for 2026 disclosure cycle.

The EBA’s latest consultation represents a deepening maturity in ESG risk oversight — one that banks must treat as a strategic opportunity, not just a compliance issue.

For ESG Book, these changes offer a clear mandate to evolve alongside the regulatory landscape: building scalable, modular, and science-aligned tools that help institutions translate sustainability commitments into transparent, auditable disclosures.