The EBA’s New Prudential Reporting ESG Rulebook

A Fundamental Shift in Banking Supervision

At ESG Book, we analyze market-moving events that reshape the financial landscape. The European Banking Authority's (EBA) latest consultation on ESG supervisory reporting is one such moment. The consultation paper sets out a proposal for new Implementing Technical Standards (ITS) for supervisory reporting, effectively embedding ESG risks into the core of the EU's prudential framework.

This is not a mere extension of existing disclosure requirements. It represents a landmark shift, moving ESG from a tick-box, disclosure-based exercise to a quantitative, data-driven component of prudential supervision, on par with established frameworks like FINREP.

Financial institutions’ ability to manage ESG risk will be publicly benchmarked against peers with unprecedented granularity. For global banks, mastering the data challenge this is no longer just a matter of compliance—it is a critical determinant of future market leadership and business model resilience.

Turning Reporting Mandates into Actionable Intelligence

The EBA’s framework demands a level of data precision and consistency that will test the limits of even the most sophisticated banking data architectures. The key challenge is well-defined: how to source, manage, and report borrower- and asset-specific data from a complex and fragmented reporting landscape. Success hinges on transforming this data challenge into a source of strategic intelligence.

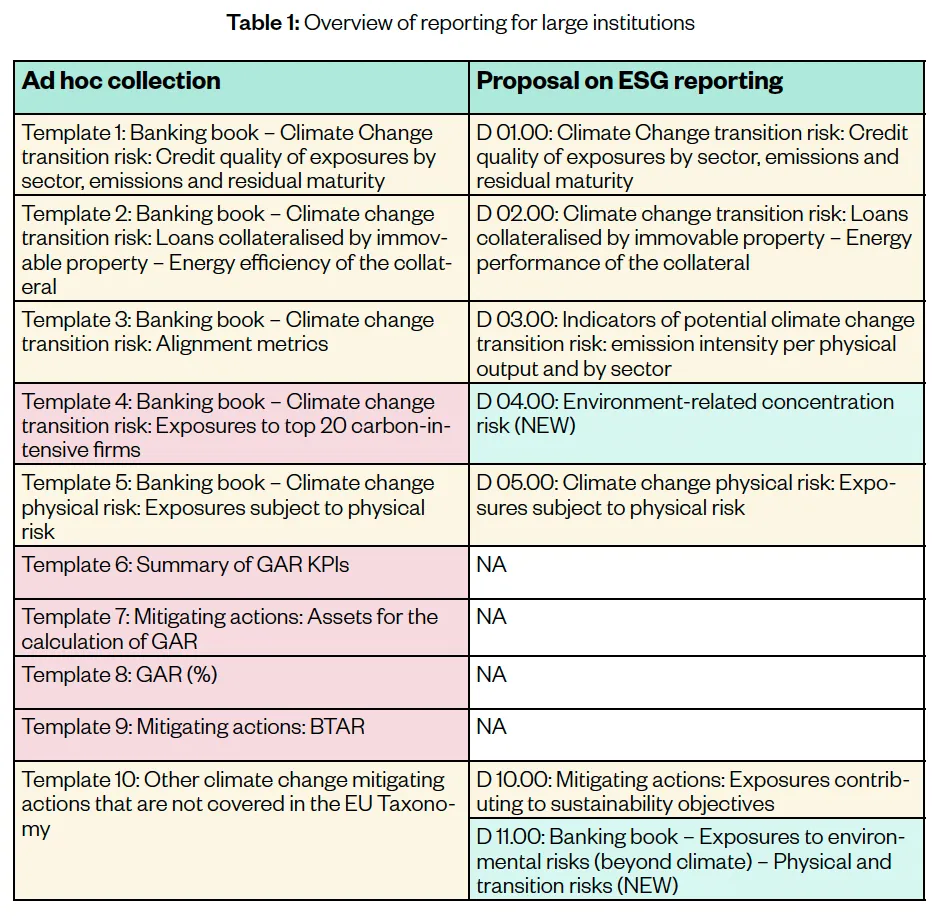

Detailed Breakdown of Key Proposed Changes

Strategic Omission: GAR/BTAR Templates Axed

A critical point within the EBA's proposal is the decision not to replicate the highly detailed Green Asset Ratio (GAR) and Banking Book Taxonomy Alignment Ratio (BTAR) templates from the previous Pillar 3 framework. This should not be misinterpreted as a signal from the EBA that Taxonomy alignment is immaterial for prudential supervision. The EBA's intention is rather to avoid duplicative reporting, as this data is already mandated for public disclosure under the Taxonomy Regulation and CSRD.

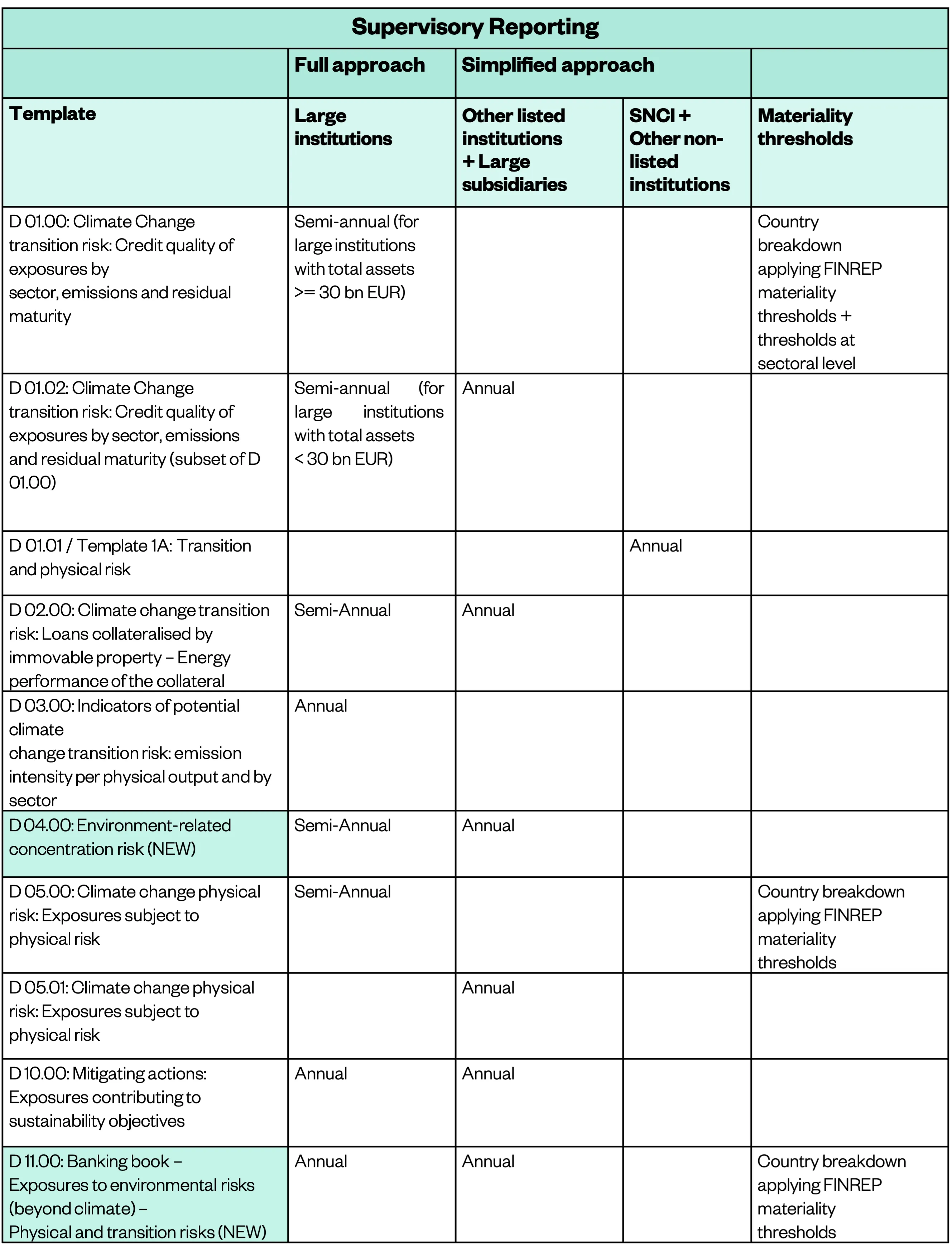

Core Principle: Proportionality in Application

The EBA’s proposal introduces a suite of new and revised templates aimed at providing supervisors with granular, comparable data to monitor ESG risks. EBA is proposing to cut reporting requirements across supervisory reporting frameworks, including ESG by approximately 50%. The framework is built on the principles of proportionality and alignment with existing regulations (e.g., CSRD), but its requirements are extensive. A tiered approach will be applied to manage the reporting burden:

- Large, Listed Institutions (LIs) (with over €30 billion in assets): will face the full reporting scope, encompassing seven detailed templates. LIs will no longer have to report GAR/BTAR as part of Taxonomy-alignment metrics but will be required instead to focus on environmental exposures encompassing physical and transition risk.

- Other Listed Institutions & Large Subsidiaries: will report using a simplified set of six templates.

- Small and Non-Complex Institutions (SNCIs) & Other Non-Listed Institutions: will have the most streamlined obligation, using a single, consolidated template (D 01.01) to report a reduced set of essential data points.

The updated EBA ESG supervisory framework is designed to be more than a reporting exercise and act as a catalyst for fundamental change.

- ESG Enters the "Hard" Risk Toolkit: By requiring ESG metrics to be reported alongside and consistent with financial data (FINREP), the EBA is integrating sustainability into core risk management. ESG factors will need to be incorporated into credit risk models (PD, LGD), stress testing, and capital planning (ICAAP).

- Data Management Becomes Mission-Critical: The granularity, consistency, and breadth of coverage of data will place immense strain on existing infrastructures. Banks must move from fragmented spreadsheets to a centralized, governed, and auditable "single source of truth" for ESG data. This is no longer optional, but a foundational requirement for regulatory compliance.

- Strategic Repositioning is Inevitable: The transparency demanded by these templates—both for supervisors and the public—will expose risk concentrations and vulnerabilities. This will force a strategic reassessment of client strategies, sector limits, and business models, accelerating the shift toward transition finance and sustainable products.

- Improved Governance and Centralized Data in a Fragmented Supervisory Landscape: The EBA is creating an EU wide public repository of all supervisory and resolution authorities’ data requests, improving transparency, supporting future streamlining, and helping banks avoid duplicate reporting. To address frequent ad hoc data requests, the EBA is developing common practices to align on how authorities design and issue them, improving coordination and reducing banks’ reporting burden.

Timeline

- Public Consultation Deadline: July 10, 2026. A critical window to engage and help shape the final, operational reality of these rules.

- Anticipated "Go-Live" Date: With a plausible reference date of mid-to-late 2027, the timeframe for building the required infrastructure is exceptionally tight.

Recommended Action Plan for Banks

- Conduct a Data-Readiness Assessment: Initiate a top-down assessment of your existing data landscape against the EBA’s granular requirements to rapidly identify critical gaps.

- Upgrade Your Global ESG Data Infrastructure: Commission your technology and data leadership to design the "collect once, use many times" architecture needed for the future of global regulation.

- Future-Proof Your Risk Frameworks: Mandate your Chief Risk Officer to begin integrating dynamic, data-driven ESG factors into the core of your global risk and capital models.

Conclusion: A Defining Moment for a Data-Led Future

The EBA's framework is a clear signal that the future of finance is data-led. As your trusted data ecosystem partner, ESG Book sees this not as a burden, but as an opportunity for the industry's leaders to separate themselves from the pack. The winners will be those who move beyond fragmented, manual approaches and embrace a technology-first, data-driven strategy. This is the moment to invest in the scalable, transparent, and robust data infrastructure that will not only ensure compliance but also unlock a new universe of insights.